There is a fear that defined contribution, 401k-style retirement plans will replace current state pension systems. While private sector employers now predominantly offer 401k plans, a recent Center for Retirement Research (CRR) report tracks the emergence of defined contribution plans and other options in the public sector. The authors find that few states have adopted pure defined contribution plans, but there has been a recent increase in the number of non-traditional retirement plans, including hybrid plans that combine less-generous defined benefit components accompanied by a defined contribution plan. These plans give employees greater money management options while reducing state financial burdens.

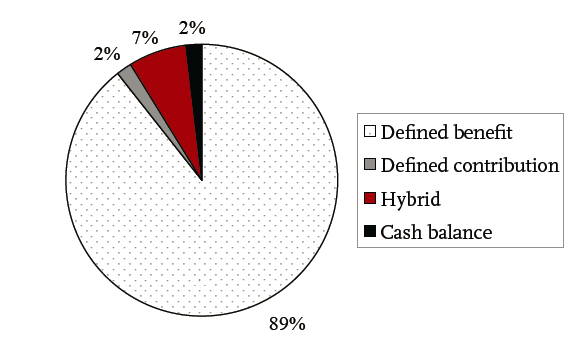

Most states retain a traditional defined benefit (DB) plan for their public sector workers. These plans offer retirement benefits set by a pre-determined formula based on service years, final average salary, and a multiplier (i.e.: the benefit is “defined”). Currently 89 percent of state and local workers have a DB plan. On the other hand, only 2 percent of state and local workers have only a defined contribution (DC) plan, or plans in which employers and employees contribute set amounts but the end benefit remains unknown (i.e.: the contribution is “defined”).

Distribution of State and Local Participants by Plan Type, 2012

Source: Center for Retirement Research; Actuarial and financial reports; and Public Plans Database (2012).

A small but growing contingent (about 11 percent) of public sector workers are enrolled in non-traditional plans including hybrid plans with DB and DC components, or another alternative plan called a cash balance plan. Cash balance (CB) plans are a type of defined benefit plan that sets an employee’s retirement benefit in terms of a stated account balance; at retirement, employees can choose whether they receive monthly payments or take their entire balance as a lump sum. Unlike traditional DB plans, CB plans increase the likelihood of making required contributions and therefore avoid large unfunded liabilities. Additionally, CB plans spread benefits more evenly between employees and therefore avoid the “back-loading” problem of traditional DB plans and are also portable.

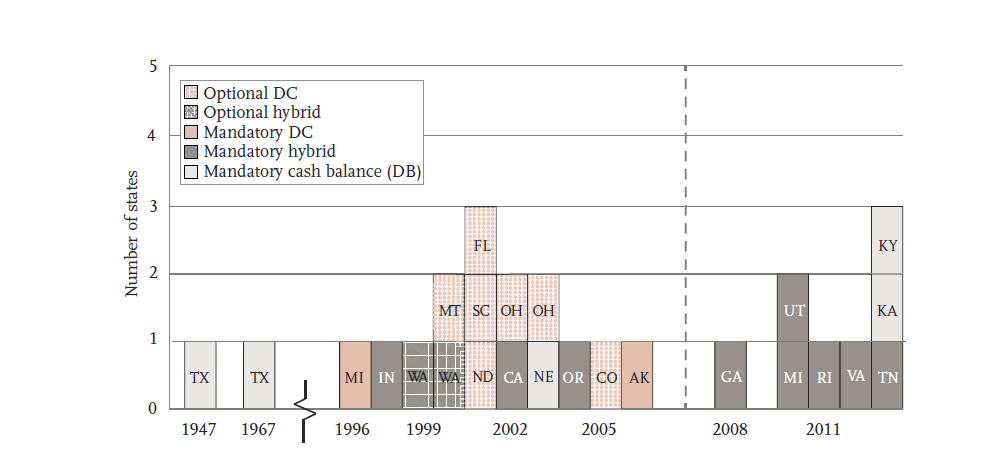

The chart below shows the adoption of defined contribution, hybrid, or cash balance retirement plans in their states through the years.

Source: Center for Retirement Research; actuarial reports; state websites; National Association of State Retirement Administrators (2013); and Munnell (2012).

As seen in the above bar chart, alternative retirement plans were virtually non-existent in the public sector except in one state (Texas) prior to the 1990s. Beginning in the mid-1990s, however, a number of states began to enact non-traditional retirement plans. From 1999 to 2004, six states created optional defined contribution plans: Montana, Florida, South Carolina, North Dakota, Ohio, and Colorado. These state plans gave public employees the option to enroll in a 401k style retirement plan. After the financial crisis in 2008, six states adopted mandatory hybrid plans: Georgia, Utah, Michigan, Rhode Island, Virginia, and Tennessee. Each of these plans included DB and DC components, usually with a smaller DB and a 401k-style DC with matching employer contributions. Two states, Kansas and Kentucky, created mandatory CB plans in 2013 that will begin enrolling new workers in the coming years.

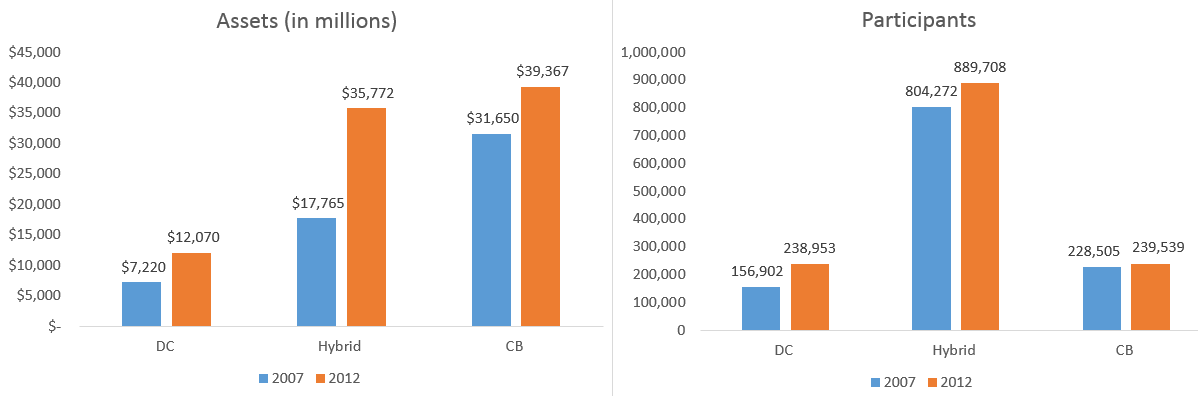

Nationwide over the last five years, the number of public sector workers enrolled in voluntary or mandatory defined contribution, cash balance, and hybrid plans combined climbed from 942,000 to over 1.1 million participants, while assets in those plans rose from a $22.9 billion to $46.6 billion. Hybrid plans alone grew from around 13.3 billion in assets to 21.9 billion from 2007 to 2012, and now have over 736,000 participants.

The following charts show the growth in total assets and participants in DC, hybrid, and CB plans over the past 5 years.

Source: Center for Retirement Research Appendix B. Assumes most recent year's assets data (2011) for Texas Muncipal TMRS.

While the majority of states retain a traditional defined benefit system, a rapidly growing cluster of states have enacted alternative plans that offer greater career flexibility to individual teachers and greater financial sustainability for state and district budgets. This trend will likely continue in the coming years.