One of the big problems with teacher pension plans is that they’re not portable. A teacher who works 30 years in the same state can expect to earn retirement benefits that are 30-70 percent higher than a peer who divides that same career into two 15-year stints in different states. The teachers, the salaries, the job, everything can be the same, but the mere fact of moving, even one time, can significantly impact a teacher’s retirement wealth.

This problem is exacerbated in the 13 states where teachers and other government employees do not participate in Social Security. These states, representing about one-third of America’s teaching work force, have made the calculation that they will be able to provide better retirement benefits to workers by investing contributions in the stock market rather than paying taxes into Social Security. That calculation may be correct for the state itself over the long run (but it doesn’t look too smart right now…), and it may mean higher benefit payouts for workers who stay in the system, but it’s certainly a losing proposition for teachers who move across state lines.

The New York Times has an interesting story about Maine’s ongoing attempt to move teachers into Social Security. It reports that only about one in five teachers in Maine stick around long enough to earn maximum retirement benefits, and the rest leave, taking neither a full pension nor Social Security benefits with them. Mobility figures are similar in other states.

The proposed changes will not affect current workers, and thus will not improve the condition of the state’s pension fund. Still, it’s a sensible solution to both improve the state’s long-term fiscal outlook while simultaneously helping out mobile teachers.

This blog entry first appeared on The Quick and the Ed.

Taxonomy:Michael Mulgrew, head of the United Federation of Teachers in New York City, suggests the city can ease its budget crisis by offering early retirement incentives for experienced teachers to retire. In today’s New York Post he writes:

Retirement incentives are particularly effective in the Department of Education, since senior teachers make more than twice the salary of entry-level teachers. There are about 25,000 experienced teachers to whom such an incentive could be offered right now. Given current salary levels, the retirement of 1,000 of them would save the city $55 million per year. If 4,000 senior teachers were to retire, the system would save more than $220 million – even if every retiree is replaced by a new teacher.

This is a common argument you hear during budget crises, but the math does not add up. Given New York City’s hiring spree over the last decade, not to mention local pressure to keep class sizes low, it’s safe to assume the retiring teacher would indeed be replaced. To get to Mulgrew’s $55,000 savings per teacher, we have to assume the district will replace a teacher that’s maxed out on the salary schedule ($100,000 in NYC) with one without a Master’s degree or any years of experience ($45,000). Mulgrew’s figure is the maximum amount and any variation (say, if the new hire had a few years of experience or additional credits beyond a bachelor’s degree) would reduce the savings. More importantly, this calculation does not include the minimum $44,000 annual pension that a retiring teacher with that level of experience would be eligible to receive. Including health insurance costs–New York covers 90 percent of retiree health expenses–would wipe out any remaining “savings” completely. This does not count any one-time payments or new early retirement incentives that might be used to encourage senior teachers to retire.

These payments do come out of slightly different pots of money, and it might be tempting during a budget crisis to play around with numbers and come up with magic savings, but ultimately that’s just dishonest.

This blog entry first appeared on The Quick and the Ed.

Taxonomy:The Foundation for Educational Choice has a new report today attempting to change the way we treat public pension plans. It essentially boils down to this: States themselves claim their pension funds covering teachers, principals, and other educators, are 78 percent funded, but the authors use different calculations based on what’s expected of private companies, derive another number and poof! the funding ratio drops to 60 percent. They then throw out the eye-boggling stat that states are actually $933 billion in the red due to unaccounted pension obligations.

Don’t believe it.

See, private pension funds are different than public ones, and they should be treated differently too. Private companies are required to contribute, on behalf of their defined benefit (DB) pension plans, to something called the Pension Benefit Guaranty Corporation (PBGC). The PBGC asks all employers with a DB plan to fully fund it so their future obligations are covered in case they ever go out of business or run out of money. When private employers fail to meet these obligations, they pay into the PBGC fund at higher levels. The PBGC can then compensate workers if their employer goes belly up. So when Enron, TransWorld Airlines (TWA), and Bethlehem Steel went bankrupt, their workers still earned some retirement benefits that had been promised them.

States, unlike private companies, do not fold under. Indiana, which according to the authors has a DB pension plan for teachers that is only 42% funded, is not likely to go out of business and take its workers down with it. The state of Indiana can assume a riskier investment return for its pension fund than an employer like those mentioned above or any other modern private firm (and, just for good measure, it’s worth pointing out that Indiana assumes only a 3 percent real rate of return).

All this is lost on the report’s authors, who would prefer states lower their assumptions on stock market returns from about 8 percent down to 6, the standard rate used by corporations in their calculations. This would mean telling a state like Pennsylvania, which has accumulated a 9.23 percent return in the stock market over the last 25 years (as ofFebruary 2010), that its 8 percent investment assumption is too high.

There are good reasons to consider changes in state pension plans, but this isn’t one of them. Expect more on this topic from Education Sector in the coming months.

Update: Stuart Buck, one of the co-authors of the study, responds here. Buck does two things wrong: One, he assumes that states are inherently bad actors willing to risk their pension money “gambling on a horse race.” That may be true in some cases, but the onus is on him to prove that all states are making such risky investment decisions, and thus need stricter rules on which they should be governed.

Two, he’s ignoring real world evidence. The document I link to above shows Pennsylvania has a 9.23 percent investment return over the last 25 years after one of the worst decades for investments on record. Buck can point to the fact that it’s down over the last five and a half years, but that’s clearly overshadowed by what’s happened in total. It seems reasonable to let a state assume what’s happened historically is likely to happen in the future. States and localities are afforded the long-term perspective, so they should be able to base their investment and interest assumptions on what’s happened over a very long horizon. The past doesn’t predict the future, but it shouldn’t be ignored either.

This blog entry first appeared on The Quick and the Ed.

Taxonomy:Question: What do you get when you add a bad stock market + equally bad state budgets + generous pension benefits + an enhancement of those benefits + rising health costs + an aging workforce?

Answer: A large unfunded liability.

Example A is Pennsylvania, which recently announced they will be increasing the employer contribution rate for retired teacher pension and health benefits in 2010-11 by 72 percent over current levels. The projections into the future are even worse, as the Public School Employees’ Retirement System of Pennsylvania (PSERS) is currently predicting the rate to nearly triple in 2012-13.

The graph below shows a 60 year look, 30 years back and 30 years forward, at employee and employer contributions into PSERS. The blue line is the percentage of salary that the average employee contributes, and it has been pretty steady over time, although it has risen slightly. The red line is the combined contribution of school districts and the state (determined by formula, but the state contributes a little more than half), and it has fluctuated wildly. It was in double digits from 1973 to 1997, hit a low of 1.09 (1.09!!) in 2002, and is expected to reside above 30 percent from 2014 to 2020.

*indicates future projection

The projections already include an eight percent annual investment gain for the next 30 years, but even after that assumption added to the large employer contributions, the state will still have an unfunded liability of over $7 billion in 2039, in present dollars. To put that in perspective, the state and all its school districts contributed only $617 million last year.

The options to fix this situation are not very appealing, nor are they unique to Pennsylvania. State and local governments could, and probably will, raise taxes. That’s pretty much inevitable, but it’s also politically unpalatable. Because pension benefits are considered a legally binding contract, the state cannot reduce benefits to current employees. So, instead, they’re likely to address the political problem by taking what amounts to mild budgetary solutions and reducing benefits or changing the retirement structures for future employees and requiring higher employee contributions. PSERS could also seek to increase its investment performance (they’ve averaged a 9.25 percent return over the last 25 years), but to do so would require it to take on more risk.

Ultimately, the state should also be thinking of long-term political solutions. Pension funds use a process called “smoothing” so that any temporary gains or losses in investment income do not force the state to swing contributions too far in one direction. This helps maintain focus on the long-term funding ratio, but it also means the state feels especially flush near the end of long bull markets, such as the technology boom in the late 1990s and the housing bubble from 2002-2007, and particularly poor after precipitous drops, such as right now. This has some serious consequences, because in 2002, feeling flush with money, the state set employer contributions at ridiculously low rates at the same time they increased benefits. A stock market crash later, and they’ll be paying for these decisions for at least the next 30 years.

Other states, like Oklahoma and Georgia, have passed laws that forbid this type of short-term thinking. Any pension bill must be proposed in one year and accompanied by an independent budget estimate. Then, the legislatures cannot give an up-or-down vote until the following year. This step injects more reason and caution into the process, and makes for a much broader discussion of retirement benefits for public sector workers.

We’re likely to see more states in the near future facing the types of choices Pennsylvania is discussing. Let’s hope more states follow the lead of Oklahoma and Georgia and begin thinking longer-term.

This blog entry first appeared on The Quick and the Ed.

Taxonomy:The Wall Street Journal had an interesting article recently about pension spiking, a practice where workers use the calculation of their pension benefits to their advantage:

Pete Nowicki had been making $186,000 shortly before he retired in January as chief for a fire department shared by the municipalities of Orinda and Moraga in Northern California. Three days before Mr. Nowicki announced he was hanging up his hat, department trustees agreed to increase his salary largely by enabling him to sell unused vacation days and holidays. That helped boost his annual pension to $241,000.

This is entirely legal, but it amounts to real money spent on the part of state and municipal retirement systems:

Mr. Nowicki recently turned 51 years old. If he lives another 25 years, his pension payments will cost the fire district an estimated additional $1 million or more over what he would have received had he retired at a salary of $186,000, not including cost of living adjustments, a fire board representative said.

And, even though Mr. Nowicki is “retired,” he is still employed by the fire department as a consultant earning $176,000 a year.

Teachers are able to take advantage of these provisions as well, sometimes through informal ways like selling back vacation or sick days, and sometimes more subtly, through their district-negotiated contracts. In my recent study of large urban district salary schedules, I discovered an interesting example from the state of Florida. In Florida, teachers are awarded retirement benefits based on their salary over their last five years on the job. So, a district that opts to pay their teachers high salaries for these five years has to compensate them slightly higher for those five years only. But the state will be paying higher retirement benefits, based on these higher salaries, for the rest of that teacher’s life.

Broward County, Fla., for instance, gives teachers an average raise of only $320 in their first 10 years on the job, but back-loads $20,000 in raises into a short time period between year 18 and 21 on the job, packing almost 40 percent of all experience-based compensation into these three late-career years, a stage when teachers are unlikely to gain effectiveness in a commensurate way. This trend has accelerated over the last decade, as teachers crossing the threshold from 20 to 21 years of experience in Broward County have netted average raises of 16.1 percent, compared to 5.2 and 6.5 percent raises, respectively, for teachers crossing the 18- to 19-year and 19- to 20-year thresholds.

This blog entry first appeared on The Quick and the Ed.

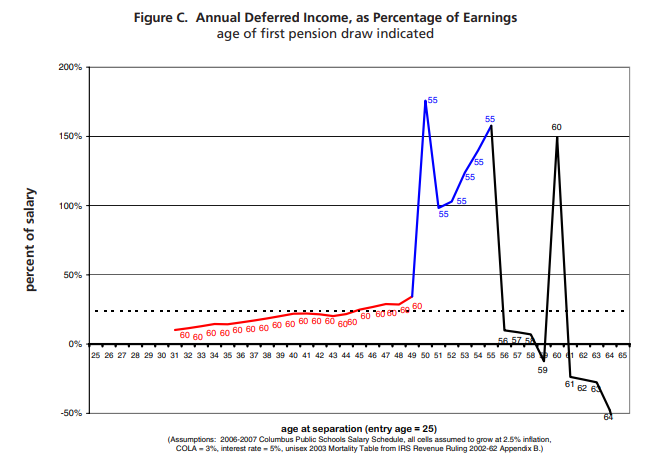

Call it the chart that launched a conference. In 2007 Robert Costrell and Michael Podgursky released a report called “Golden Peaks and Perilous Cliffs: Rethinking Ohio’s Teacher Pension System.” The report, and the attention spawned by it (including a dedicated research conference), was driven by one chart.

The chart shows the retirement wealth accrual over time for teachers. The report’s title is evocative of the chart; namely, it demonstrates vividly the enormous financial pressure teachers face at various stages of their careers. Podgursky, Costrell, and others have since drawn similar charts for a number of states, and they all show how teacher retirement accounts grow slowly over time, only to spike dramatically at various ages determined by state pension plan formulas. Ohio’s, the first of the state charts and the one below, has two such spikes, one for an early retirement incentive and again at the “normal retirement age.” In the chart below, the hypothetical teacher who enters teaching at age 25 gains over $100,000 in future pension wealth at age 50, 55, and 60. Every year they choose to work past age 60, they forfeit pension wealth, meaning they’re actually losing money by working additional years.

Not surprisingly, these peaks correspond neatly to retirements: teachers do respond to the incentives, and they are, for the most part, retiring when the retirement formulas tell them to do so. Research from California shows that teachers changed their retirement age to 61.5 (an unusual retirement age) in response to changes in the state’s retirement structure in the late 1990s. In an era when Americans in general have been retiring at later ages (due to declines in average pension and Social Security wealth), teachers have been retiringyounger.

So there I was spending two days in Nashville discussing these peaks and how, if, or whether they could/should be fixed. With the Dow and the S&P 500 plunging to six-year lows, it was an interesting time to be having the discussion.

With only a few exceptions, most teachers have defined benefit (DB) pension plans. This means they are guaranteed retirement benefits determined by a formula, which are almost always derived by multiplying some replacement factor (typically 1-3%) times years of service times average final salary. If a teacher lived in a state with a constant replacement rate of 2% and retired after 25 years on the job with a final average salary of $50,000, her benefits would look like this:

Monthly benefit = (.02 X 25 X 50,000)/ 12

Monthly benefit = $2,083.33DB plans were once common in the private sector too, but their frequency has fallen since the mid 1970s. They have been replaced by defined contribution (DC) plans. DC plans, like their name, define the retirement contribution an employer makes on an employee’s behalf. In most DC plans, the employer contributes a certain percentage of an employee’s wages into a 401(k) account.

The conference at times devolved into a DB versus DC debate, but before I get into why that’s a false choice, I’ll take some time to weigh their strengths and weaknesses.

DB plans allow individuals to make predictable estimates of their retirement wealth. Since they are usually accompanied by cost-of-living adjustments, they should not erode significantly because of inflation. They last until the individual passes away. They pool risk, so that the fund can make wise, long-term investments. And when a recession hits, current teachers and all taxpayers bear the responsibilities of DB benefit promises. If their goal is to provide a secure retirement as a reward for a career of service, they do their jobs.

At the same time, DB plans transfer wealth from mobile workers to non-mobile ones (mobile workers contribute but never capture the full benefits that longevity assures), from young to old (the young pay into a system that backloads rewards), and from men to women (women live longer and thus earn benefits for more years). (As an aside on teacher quality, DB plans promise nothing to prospective teachers who want to try out the profession. If they leave before being “vested,” usually after five or ten years, they get nothing.) State-run DB plans are subject to interest group influence, which has caused rising payout rates and given teachers more generous pensions over time, especially when compared to private-sector workers. Worst of all, public sector DB plans are typically locked in. A state that increases pension benefits during boom times cannot rescind this offer during boom cycles. In fact, in many states, pension benefits can never be reduced from the time a teacher begins their career.

DC plans offer an alternative. They give every employee the same percentage of salary contribution. In this way, they make it much easier for employers to project future obligations. Individuals have choices; they can participate if they want to or not, invest as they please, and take the money with them when they leave. There is no “maximum” DC pension wealth, because the contribution stays the same regardless of age or service. If a teacher passes away prematurely, her heirs inherit what remains of the account.

Or, the money in a DC plan could run out. Individuals tend to do a bad job of investing, not saving enough, not diversifying their portfolio, investing in too risky or too conservative assets. DC plans are also subject to the whims of the business cycle, since an employee must reduce risk as they near retirement. All of these factors make DC plans less efficient; DB plans often earn investment returns one to two percentage points higher than DC participants.

Ultimately, the DB plans suffer from two main things. One is the aforementioned peaks, and the other is portability. Both are fixable.

The peaks of the current systems are a serious problem. They pull bad teachers to stay in the profession too long, just so they’re able to earn a full pension. And they push out teachers who want to stay in the profession, because of the severe financial penalties on teachers who opt to stay in after their “normal retirement age.” But peaks are not unique to DB plans. Employees with DC plans time their retirement decisions to coincide with high market values of their accounts. Alternatively, we’re now seeing stories of people delaying retirement because of current economic conditions. Of the two, DB plans are the ones that are not inherently linked to peaks.

Politicians like to reward active interest groups with tangible benefits, especially if those benefits are obligations only at some time in the future. Teacher pensions fit this precisely: their unions have significant influence on state politics, and a promise for pension benefits accrues to members slowly over time. Current politicians saddle future ones with the budget problems while satisfying an interest group. In an analysis of the actions of Missouri’s state legislature, which increased teacher pensions nine times during a ten-year period from 1991-2001 (netting each teacher about $75,000 in future benefits and imposing a $5.4 billion long-term liability to the state), researchers saw little evidence of any real analysis. The economy was running smoothly, so state legislators spent as if there were not going to be tech or housing bubbles looming in the next decade.

Other states have taken similar paths, making reform seem impossible, but two states have experimented with legislation that has introduced sanity to the process. Oklahoma and Georgia now have laws on the books requiring a two-year deliberation period before making any changes to the state pension plan. The state must create an analysis at the front-end of the impacts of the proposal, update the analysis after an additional year, and then pass the legislation. Legislators are no longer able to commit the state to large future budgetary obligations without two full years of deliberation.

The second problem with DB plans is interstate portability. Because benefits accrue slowly over time, a teacher who splits her years of service between two states will earn a significantly smaller pension than someone with the same number of years of service in only one state. Researchers at the conference found a hypothetical teacher with 15 years of service in each of two states would accumulate 35-65% less pension wealth than one who stayed put. Thus far, mechanisms to increase portability mostly fail. Teachers can cash out of the first pension program to purchase additional years of service, but in the process they often must forfeit all of the employer’s contributions in the process. These are substantial sums, since employers often contribute the majority of the fund. Some states even mandate the teacher forfeit any earned interest.

But these rules are not fixed in stone. In reality, these prohibitive rules are in place for nothing other than to enrich the state fund on the backs of teacher-leavers. States have no real incentive to fix them now, but they could form partnerships across borders to agree to more equitable rules for interstate movers. If this didn’t work, the federal government could threaten a pension fund’s tax-exempt status if it refused. Or, employers could begin offering a form of DB plan called cash balance (CB). CB plans guarantee individuals a (generally low) return on their investments and typically require the employer to contribute some percentage of the employee’s salary. The account is in the employee’s name, but the benefit–the interest rate and contributions–are guaranteed, placing the risk with the employer. An employee can choose whether to take the account balance as a lump sum payment or transfer it to a lifetime annuity.

Ultimately, the peaks and portability problems are the largest barriers to the status quo. Because while defined benefit retirement plans for government workers often come under scrutiny for being too generous(including and especially those of teachers), it’s important to think about the goal of any retirement system. Defined contribution plans might be better if the goal is to minimize cost and risk to the employer while giving the employee maximum flexibility. But if it is to create a loyal workforce with the prospect of a secure retirement, then defined benefit plans are quite successful.

This blog entry first appeared on The Quick and the Ed.

Taxonomy: