As I write in a new piece for RealClearEducation, “When advocates for traditional defined-benefit pensions say things like, “pension plans would be in better financial shape if states made their required contributions,” that’s true, but only half the story. The other half is that the current structure carries no cost for politicians who make pension promises but fail to live up to them.” Two very different politicians—Chris Christie in New Jersey and Martin O’Malley in Maryland—are following nearly the same playbook on pensions. In response to under-funded pension plans, both cut benefits for new teachers, both made promises to raise state contributions in order to prevent future under-funding, and now both are trying to back away from those promises.

It’s an old story that politicians make promises they don’t intend to keep. But it’s worth noting that these two politicians, who are both vocal good government types, are struggling to keep promises that are only a couple years old. Pension funding isn’t exciting and it doesn’t provide any immediate return. Pensions are an investment in the future, but politicians can’t resist the urge to use today’s money to pay for today’s services.

As I conclude in the piece, "Teachers across the country must stop enabling this system, which is bad for their personal retirement and also for their profession. Instead, they should insist that all forms of compensation—including retirement benefits—are paid for upfront and that benefit promises are matched by real contributions." Read the full thing here.

Taxonomy:Pensions provide us with more than just financial data. While retirement systems collect crucial information on investments, salaries, and retiree wealth, they also provides us with key information about the characteristics of the teaching workforce: the expected number of teachers remaining in the classroom versus the number of teachers leaving the profession. In other words, pensions give us a snapshot of teacher retention.

Furthermore, not only do states and districts publicly release retirement data for the current fiscal year, actuarial reports are released annually and reach back for decades, and in many cases even more.

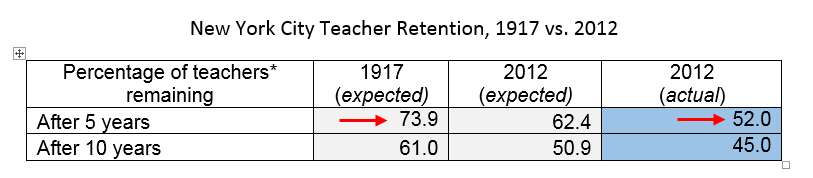

As a case example, let’s take a look at New York City. As Chad Aldeman discussed in a previous blog post, currently, half of all New York City teachers will not reach ten years of service. I used the same methodology to calculate the historical retention rates for New York City teachers from 95 years ago. The table below shows the retention rates of teachers from 1917 in comparison to retention rates in 2012.

The biggest dip in retention follows for teachers remaining after five years. In 1917 three-quarters of teachers remained after 5 years, compared to half of teachers remaining after 5 years today. Retention similarly dips at the 10 year mark of teaching from 1917 to 2012. New York City teachers today do not remain in the profession as long as they did 95 years ago.

Pensions systems have been often described as anachronistic and unfit for the current labor force. The pensions system has been in operation since 1894 in New York City. The original New York City Teacher Fund was established in 1905, and after becoming insolvent and declaring bankruptcy, was re-organized and replaced by the Teachers’ Retirement System of the City of New York. Today, a teacher in New York City must stay in the classroom for at least 10 years to receive a minimum pension. But as the data shows, only a small percentage of teachers today will actually stay long enough to meet pension requirements. More teachers are moving across jurisdictions or out of the profession altogether. New York City teachers have become more mobile, while their pension plans have not. What was established over a century ago may no longer fit the demands of today’s transient labor force.

The New York City actuarial reports, and similar historical pension data, can help researchers better understand the original design of the pension system as well as track shifts in teacher retention. In turn, we can get a fuller picture of the teaching labor force and how it has evolved over time.

*All assumptions rates are based on 25-year-old female teachers. Retention data was also collected from the 1918 and 1919 Teachers’ Retirement System of the City of New York annual financial reports, and showed similar trends as the 1917 retention rates. The reports have been digitized by Google and can be accessed from the Hathi Trust Digital Library.

Last week I presented our new paper, Friends without Benefits: How States Systematically Shortchange Teachers' Retirement and Threaten Their Retirement Security, at the 39th annual conference of the Association of Education Finance and Policy (AEFP). For those of you who couldn't make it, I've pasted my slides below and added a bit of explanatory commentary.

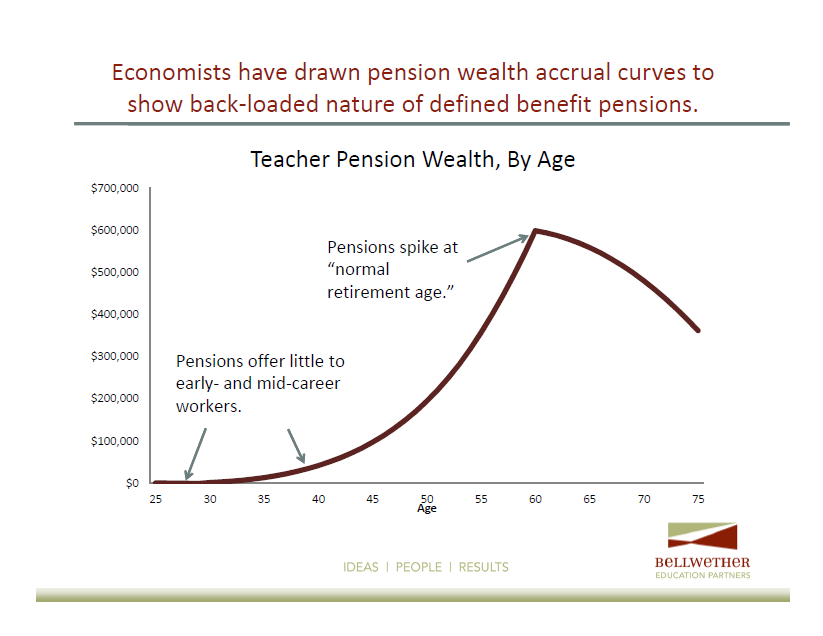

Economists like Bob Costrell and Mike Podgursky have been drawing pension wealth accrual curves for several years now. In one chart, they tell the compelling story of the back-loaded nature of defined beenfit pension plans.

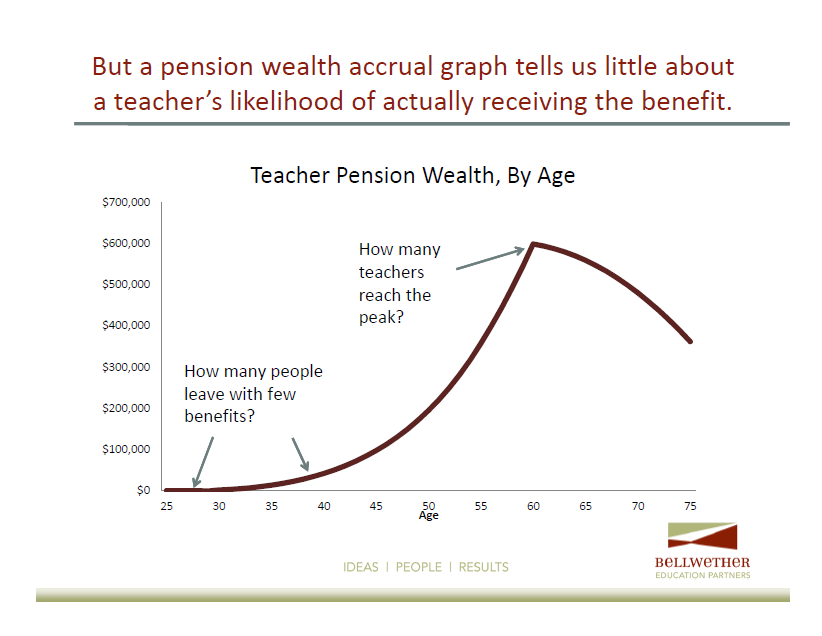

Unfortunately, the pension wealth accrual curves don't tell us much about how many people make it to each stage. If the vast majority of workers remained in one pension plan for the life of their career, the back-loaded nature of defined benefits would create some perverse incentives around the normal retirement age (where pension wealth comes to a steep spike), but it wouldn't matter that the employee was accumulating very little early in their career.

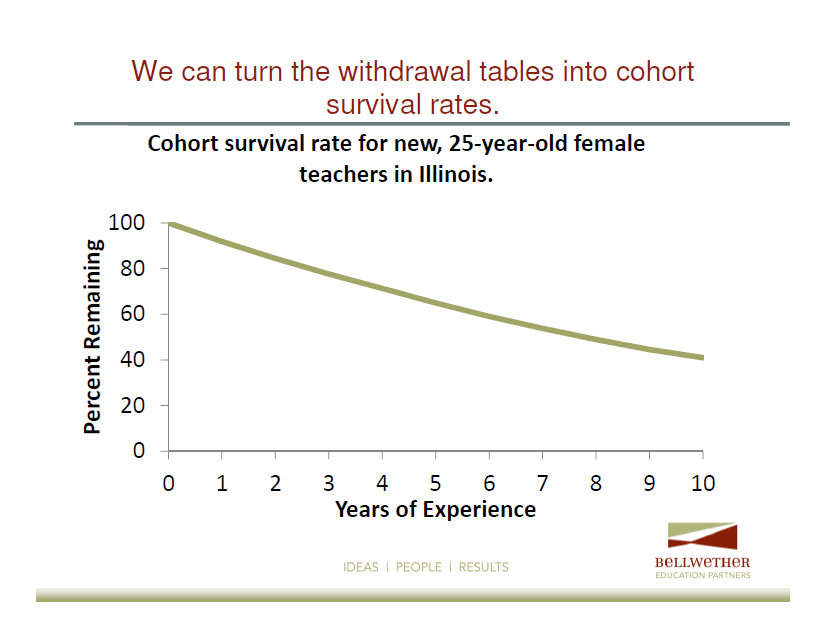

We set out to answer the question of how many teachers reach various career stages. Nationally, there's solid research evidence that slightly under half of all new teachers stick around for at least five years, but there hasn't been a good source of state data. But pension plans have this information. Pension plans need to estimate how many people will remain in the pension plan and for how long in order to estimate how much future benefits will cost. These estimates can be converted into teacher retention rates.

All states publish "withdrawal" assumptions estimating what percentage of teachers will leave in a given year. They publish separate rates based on gender, age, and years of experience, but years of experience is often the dominant factor.

We collected these tables for every state and used them to calculate teacher retention rates.

We used each states' own estimates to calculate teacher retention rates across an entire working career. In our paper we focused on new 25-year-old female teachers, but we could have run similar calculations for 47 year-old-males, for example.

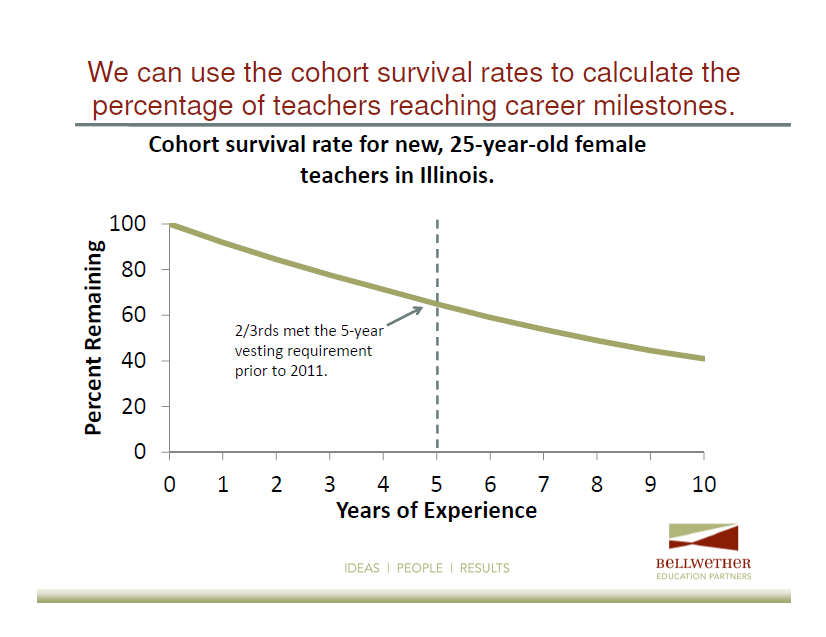

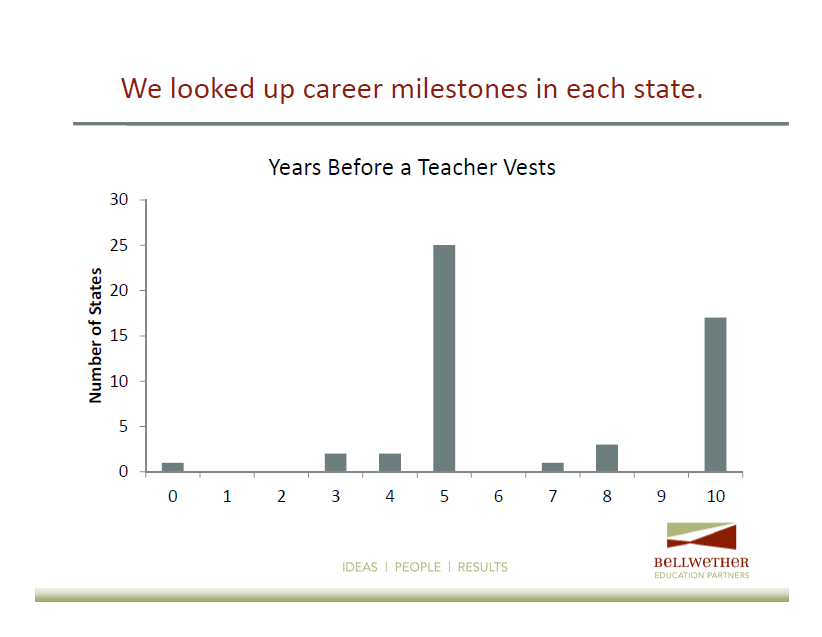

We compared the retention (aka cohort survival) rates in each state with various career milestones. In particular, we were interested in the percentage of teachers who remained long enough to "vest" into the state pension system and thereby qualify for at least a minimal pension benefit, and the percentage who remained in teaching for an entire career.

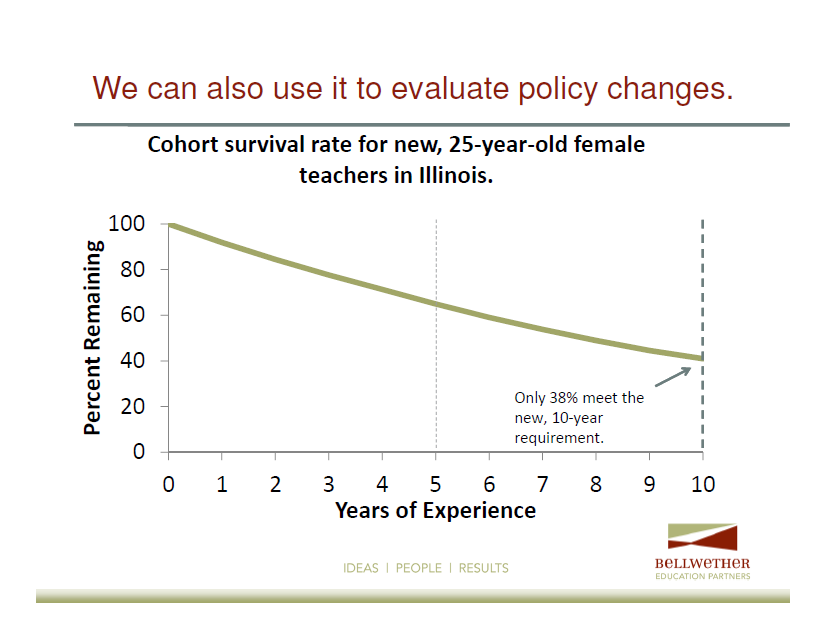

We can use these calculations to evaluate policy changes. When Illinois lengthened its vesting period from five years to ten, for example, it made it harder for teachers to qualify for a minimal pension benefit. Using the states' own figures, we estimate that only about 38 percent of teachers will remain as teachers in Illinois long enough to qualify for the new, ten-year vesting period. 62 percent of new Illinois teachers won't earn a pension from their pension system.

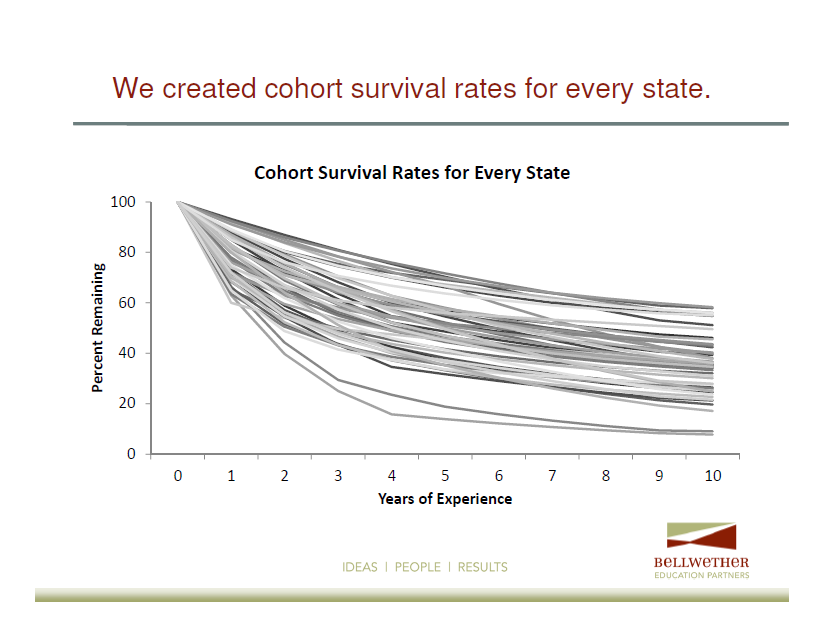

We can run these calculations for every state. The graph below shows what the 10-year retention rates look like according to each state's pension plan. The graph below isn't fine-grained enough to show the results for each state, but it does show that some states have much steeper teacher turnover rates than others.

Next, we compared the teacher retention estimated with career milestones in each state. For example, 24 states and the District of Columbia have 5-year vesting requirements, while another 17 states have 10-year vesting periods. These numbers are rising and moving to the right of the graph; during the recent recession, 12 states made it more difficult for teachers to qualify for a pension by raising their vesting requirement.

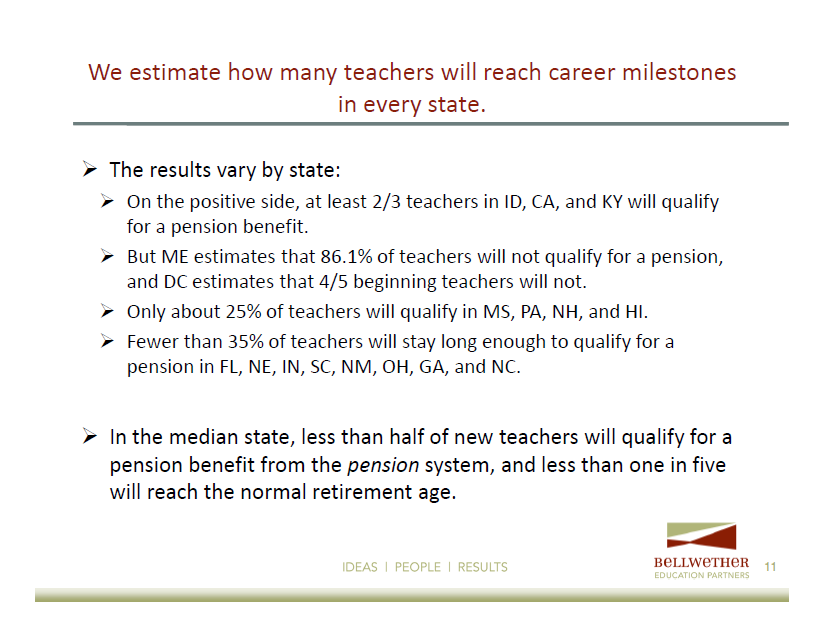

While the numbers vary by state, in the median state, less than half of all new teachers will not remain long enough to qualify for a pension. If we look at a longer time horizon, less than one in five new, 25-year-old teachers will remain as teachers for a full career and reach the state's normal retirement age.

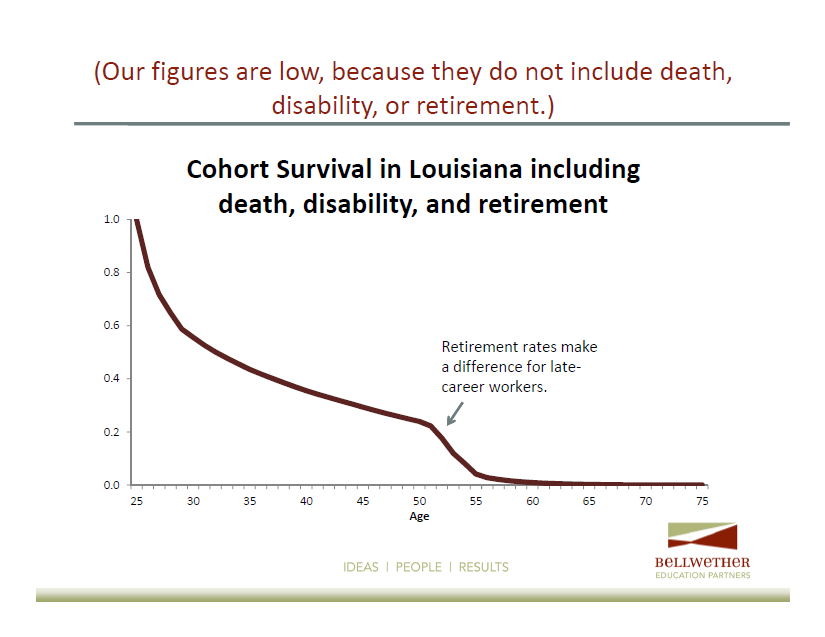

Our estimates do not include the possibility of death, disability, and retirement. Those factors would all increase teacher turnover rates, meaning our estimates, particularly those for the percentage of teachers reaching later milestones, are likely on the low end.

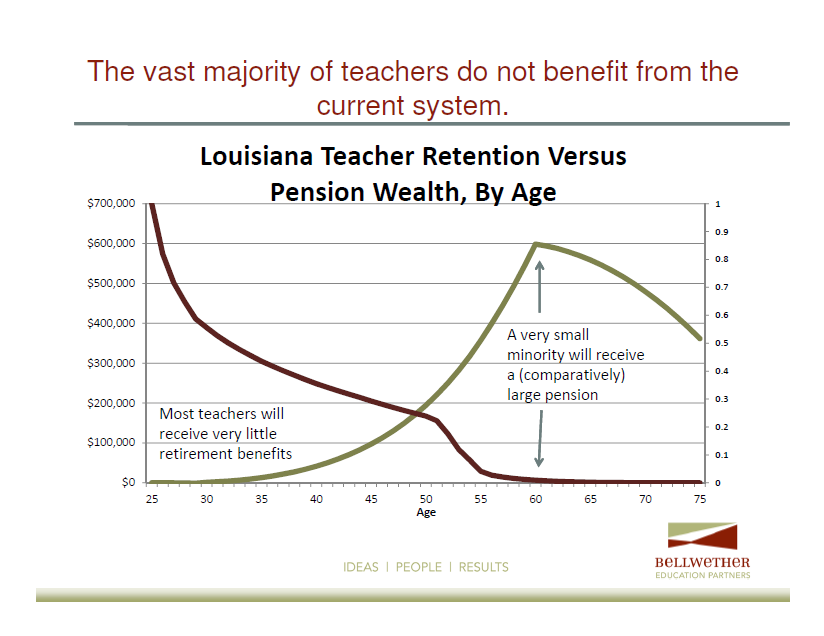

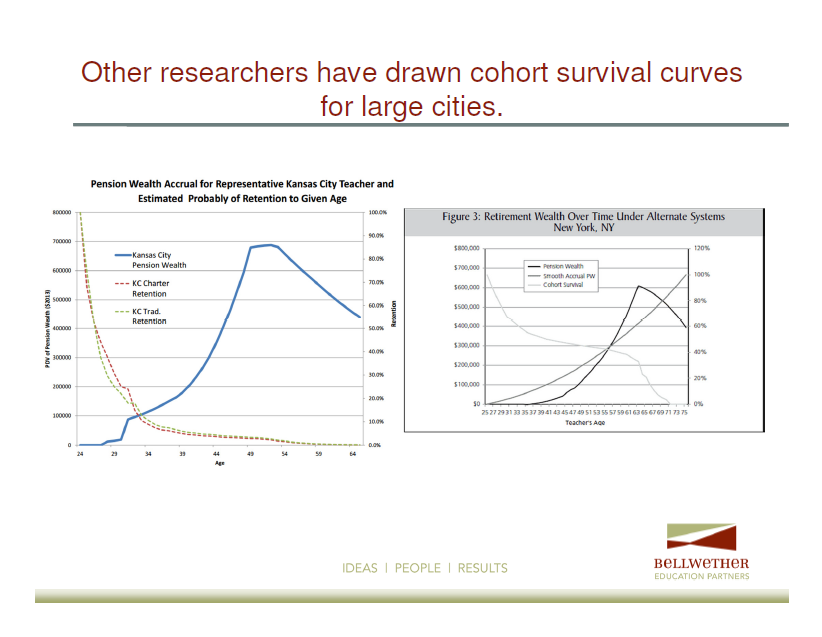

We can combine the pension wealth accrual curves discussed above with the estimated teacher retention rates. The graph below is from Louisiana. It shows that only a small fraction of teachers will remain long enough to qualify for the more generous benefits at the back-end of a teacher's career.

We aren't the first to do this type of work. Other researchers have drawn similar graphs for the 10 largest cities and for urban teachers in Missouri. They tell a similar story. But, our paper is the first to attempt to calculate these rates for every state.

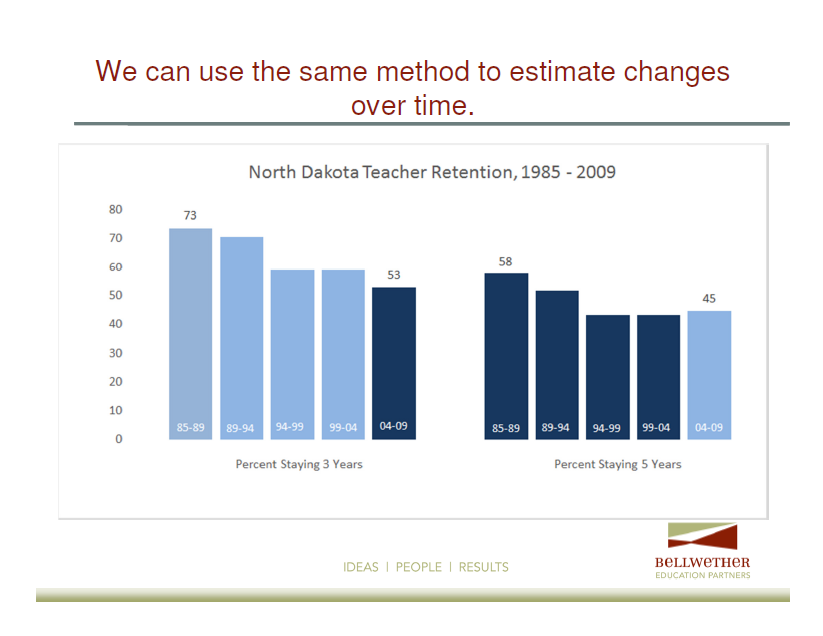

While not in our paper, here at teacherpensions.org we've used a similar methodology to study other issues. For example, in the chart below we used 25 years of data from the North Dakota teacher pension system to show how falling teacher retention rates have led to fewer teachers qualifying for a pension. North Dakota also raised its vesting period from three years to five, making it even more difficult. We estimate that, while 73 percent of North Dakota teachers qualified for a pension in the late 1980s, now only 45 percent of teachers do.

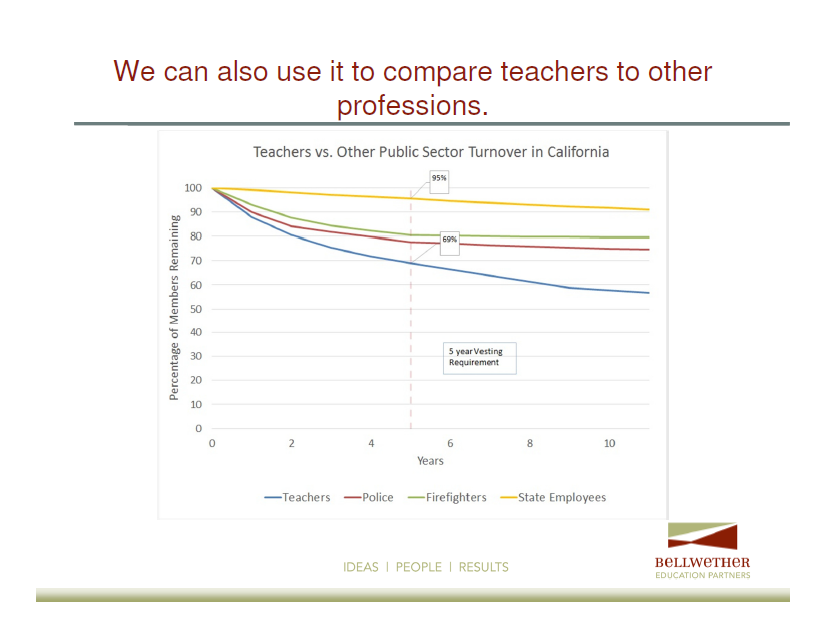

We can also use the same method to compare teacher turnover with turnover rates in other professions. The graph below compares California teachers with California police officers, firefighters, and state employees. It shows that teachers have much steeper turnover rates in California than these other professions, which suggests that the back-loaded defined pension structure is less suitable to teachers than other public sector workers.

If you've read this far, we hope you keep coming back for more information on teacher pensions as we continue to write and blog about the issue.

Warren Buffett's latest letter to shareholders of Berkshire Hathaway, the Omaha-based holding company Buffett turned into the 9th-largest public company in the world, has a wonderful primer on pensions. It's not from today and it's not directly about public-sector pensions--it's actually a 1975 memo Buffett drafted to Katharine Graham, then-Chairman of The Washington Post Company about her company's pension*, but it has a number of lessons for today.

On the irreversible nature of pension promises:

The first thing to recognize, with every pension benefit decision, is that you almost certainly are playing for keeps and won't be able to reverse your decision subsequently if it produces subnormal profitability....So rule number one regarding pension costs has to be to know what you are getting into before signing up. Look before you leap. There probably is more managerial ignorance on pension costs than any other cost item of remotely similar magnitude. And, as will become so expensively clear to citizens in future decades, there has been even greater electorate ignorance of governmental pension costs. Actuarial thinking simply is not intuitive to most minds. The lexicon is arcane, the numbers seem unreal, and making promises never quite triggers the visceral response evoked by writing a check.

On the deceptive arithmetic in pension promises:

If you promise to pay me $500 per month for life, you have just expended - actuarially, but nevertheless, in a totally tangible sense - about $65,000. If you are financially good for such a lifetime promise, you would be better off (if I have an average expectancy regarding longevity for one my age) handing me a check for $50,000.

On the hidden nature of pension costs:

Pensions costs in a labor intentive business clearly can be of major size and an important variable in the cost picture, particularly in a world characterized by high rates of inflation. I emphasize the latter factor to the point of redundancy because most managements I know - and virtually all elected officials in the case of governmental plans - simply never fully grasp the magnitude of the liabilities they are incurring by relatively painless current promises. In many cases in the public area the bill in large part will be handed to the next generation, to be paid by increased taxes or by accelerated use of the printing press.

On the difficulty of pre-funding pension plans (defined benefit pensions are intended to be forward-funded, that is, they should have sufficient assets today to pay the required liabilities tomorrow):

When salaries move ahead at a substantially higher rate than investment returns and benefits are tied to final salaries (or, even more expensively, cost-of-living increases after retirement as in recent rubber and aluminum contracts), it is virtually impossible to pre-fund obligations. Like it or not, you become much like the Social Security Fund, absent the power to tax. Should that occur, future purchasers of the products of the company must be willing to do so at prices that reflect not only the wages of current workers, but the promises to past workers.

On investors (or pension plans) seeking to outperform the stock market average:

A little thought, of course, would convince anyone that the composite area of professionally managed money can't perform above average. It is simply too large a portion of the entire investment universe. Estimates are that now about 70% of stock market trading is accounted for by professionally managed money. Any thought that 70% of the environment is going to substantially out-perform the total environment is analogous to the fellow sitting down with his friends at the poker table and announcing: "Well, fellows, if we all play carefully tonight, we all should be able to win a little."

The one area Buffett got wrong was his worry about persistent periods of double-digit inflation. Inflation was high when Buffett was writing his letter in the mid-1970s, and stayed high through the rest of the decade, but it has been relatively low since the early 1980s.

Read the whole thing starting on page 118 here.

*The Washington Post's company pension performed very well thanks to Buffett and his memo. As of late 2013, it was 140 percent funded, meaning it had accrued $604 million more than it owed.

Taxonomy:This post is a guest blog from James V. Shuls, Ph.D., the director of education policy at the Show-Me Institute, which promotes market solutions for Missouri public policy.

In Missouri, students in unaccredited school districts can now choose to enroll in neighboring accredited school districts. Some students who have elected to leave their struggling school now find themselves riding a bus for more than two hours a day. This has led many to question the school transfer idea and look for alternative solutions. Some have begun to ask, “What if instead of busing students from failing school districts to accredited ones, we bused great teachers from accredited schools into the failing districts?” It is an idea that has won a fair amount of attention.

Last November, the Cooperating School Districts of Greater St. Louis pitched the idea of providing high-quality teachers as instructional coaches in struggling schools. A similar idea was raised by CEE-Trust, the consulting firm that the Missouri Department of Elementary and Secondary Education hired to address problems in the Kansas City School District. The CEE-Trust proposal called on accredited school districts “to play a significant role in helping [unaccredited] systems improve.” The St. Louis Post-Dispatch heaped praise on this idea, calling it among the “more promising ideas.”

However, there is one easily overlooked obstacle standing in the way of turning this localized version of a teacher peace corps into a reality in Missouri’s two biggest cities: the incompatibility of different pension systems.

With the exception of Saint Louis and Kansas City, which have autonomous pension systems, all of Missouri’s school districts are part of the Public School Retirement System (PSRS). If a teacher moves from PSRS to one of the city plans, he or she will incur a significant loss in pension wealth. Koedel, Ni, Podgursky, and Xiang, economists at the University of Missouri and authors of a recent report from the Ewing Marion Kauffman Foundation, put it this way:

Consider two teachers who work thirty-year careers in the profession. The first teacher works all of her thirty years in a single plan. The second teacher works fifteen years in one plan and then fifteen years in another. Because of the way pension wealth accrues in these plans, the latter teacher will have less than half the pension wealth of the former teacher at age fifty-five.

Though this may sound like a Missouri problem, it has bearing nationwide. As the Kauffman report notes, Missouri’s separate pension systems are “a microcosm of larger national issues concerning teacher pension systems—particularly the ability of teachers to move between systems.”

Just as teachers in Missouri cannot move between pension boundaries without incurring a financial penalty, teachers cannot move across state pension boundaries without incurring similar costs. Which means, a charter operator with campuses in multiple states, like KIPP, Uncommon Schools, Achievement First, or Rocketship Education, cannot freely move a teacher or school leader between their schools in various states. Indeed, these systems punish all teachers who move from one state to another.

Koedel, Ni, Podgursky, and Xiang liken the costs associated with switching between pension systems to a tariff, “Rather than promoting free trade and labor mobility, the pension plans effectively are imposing a tariff on the import or export of human capital between” the separate pension systems.

This “tariff” on labor is not a new problem, but a longstanding one that Saint Louis and Kansas City have been struggling with for years. Prior research has demonstrated that the separate pension systems create a barrier to recruiting school leaders into the two urban school districts. The separate pension systems also limit the pool of teachers who are willing to work in the cities. Jeffrey Kuntze, chief operating officer of the Confluence Charter Schools in Saint Louis, says “the separate pension systems make it extremely difficult for us to recruit veteran teachers from the county. We can get them when they retire, but not mid-career.”

Missouri’s pension boundaries would make it practically impossible for high-performing school districts to operate a program, run a school, or loan teachers within the Saint Louis or Kansas City boundaries, just as state pension boundaries would make it impossible for schools to effectively work across state lines. They simply could not move teachers or school leaders across pension boundaries without making them suffer great financial penalties.

The only real way to solve this problem is to close the current systems to new entrants and place them in a new, statewide system that participates in Social Security and has smooth wealth accrual. Before this idea causes mass hysteria, let me stress that this would not affect current employees’ or retirees’ pensions. They would remain secure in their current system. It would, however, remove the artificial pension boundaries and allow us to create a better pension system for teachers and students.

Opponents of this idea claim that closing the current defined benefit systems would be financially unsound, as it would lead to considerable “transition costs” that would far outstrip any benefits that we may receive. This is the very issue tackled in a recent Show-Me Institute policy study by Andrew Biggs, a resident scholar at the American Enterprise Institute. Biggs examines the evidence for “transition costs” and concludes that the concerns are “largely mistaken and should not stand in the way of public employee pension reforms.”

Whether you believe busing teachers into failing schools is a viable solution or just another feel-good proposition, fixing this pension problem should be a top priority for Missouri and other states throughout the country. Missouri should not have a system that puts our neediest communities at a disadvantage when it comes to recruiting talented teachers and states should not impose a tariff on attracting quality teachers and school leaders.