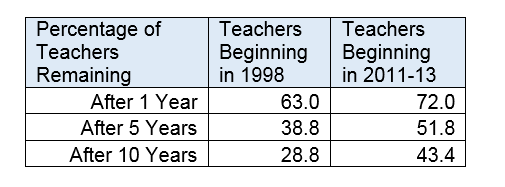

Today, roughly half of Michigan’s new young teachers will leave the classroom after five years. That may sound low, but Michigan’s retention rates are actually higher than they used to be. Fifteen years ago, even fewer teachers stayed in the classroom than they do today. The following chart shows the retention data calculated based upon the state pension plan’s assumptions for 25-year-old female teachers in Michigan.

Looking vertically within a given cohort, retention decreases over a time. Of the cohort of 25-year-old females that began in 1998, for example, the pension plan estimated 39 percent would remain after five years and only 20 percent would remain after 30 years of teaching.

Looking across the decade, however, there is an increase in the overall expected retention rates. In 1998, Michigan’s pension plan assumed only 39 percent of teachers would remain after five years. A steady trend toward higher retention continued in subsequent years, and the state now assumes that 52 percent of 25-year-old female teachers will stay five years. The change represents an increase of about 34 percent more teachers staying in the classroom at least five years.

Rising teacher retention rates is a good thing for the individual teachers as well as for their students, schools, and districts. In terms of pensions, though, rising retention rates mean higher costs. Coinciding with the increase in teacher retention, Michigan’s underfunded liability quadrupled over the past decade from $6 billion to $24 billion. More teachers staying in the systems meant higher costs for the system; the state estimated an actuarial loss of over $21 million from a decrease in withdrawals (from resignations and death) in 2009 alone.

Having half of your teachers leave the classroom within five years is nothing to boast about. But it is an improvement from past years. Michigan should continue to encourage teacher retention, and in doing so, should consider the consequences for schools, teachers, and the retirement system.

New public sector workers are getting a raw deal. States have responded to their pension funding gaps by cutting retirement benefits for new hires and increasing the amount of time workers need to serve before qualifying for a pension, raising the normal retirement age, and reducing benefit formulas.

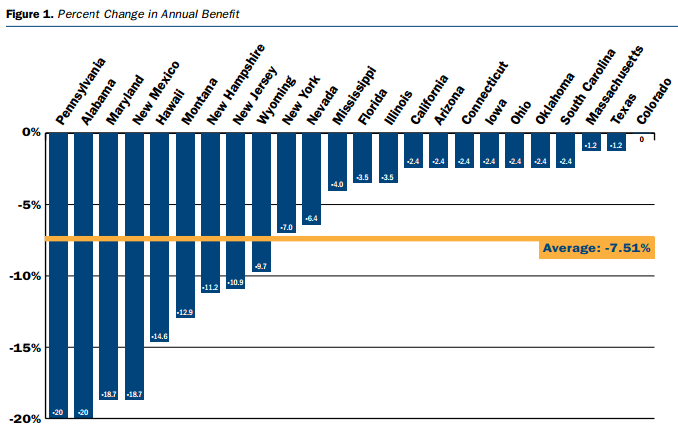

A new paper from the Center for State and Local Government Excellence and the National Association of State Retirement Administrators estimates the size of these penalties. The authors estimate that states trimmed pension benefits by an average of 7.5 percent for workers planning to stay for a full 30-year career. (The differences are likely even larger for the vast majority of workers who will never reach 30 years, but the study doesn’t mention this group.)

The chart below shows the extent of the cuts for full-career workers. The blue bars represent the difference in annual retirement benefits for equivalent workers with 30 years of experience hired pre- and post-recession. In states like Pennsylvania, Alabama, Maryland, and New Mexico, legislators cut benefits for new workers by 19 or 20 percent. New employees will have to work years longer in order to qualify for equivalent benefits.

In making these changes, states mostly shielded current employees from any cuts, instead imposing steeper reductions on new employees, the ones who will start government work in the coming years. Nothing is different about these workers except the year they were hired, and usually that’s as arbitrary as a given date. Teachers hired on December 31, 2013 may earn one set of benefits, while those hired one day later, on January 1, 2014 earn much less. They’ll be doing the exact same job and, in most states, they’ll pay the exact same contribution rates.

We shouldn’t have this problem in the first place. Unlike Social Security or other pay-as-you-go plans, state pension plans are intended to be forward-funded so that all future obligations are covered by assets today. But that’s not the way they’re working. In practice, every state is asking its youngest workers to pay for the retirement of the older workers. For example, New York State now has six different pension tiers, and each one is less generous than the one before it.

Moving to New Models

After documenting the extent of the cuts, the paper then turned toward analyzing five new “hybrid” retirement plans that combine a less-generous defined benefit plan with a defined contribution, 401(k)-style component. The authors found that three out of the five hybrid plans—those offered in Utah, Rhode Island, and Tennessee—would yield a retirement benefit that was greater than the prior defined benefit plan while simultaneously offering employees greater mobility and control. Two states, Georgia and Virginia, had such meager employer and employee contributions in the defined contribution component of the hybrid that employees were likely to be worse off financially.

(These results confirm well-structured hybrid plans can accomplish simultaneous goals of providing workers with secure retirements and more flexible working lives. The authors also interviewed state retirement officials, and interviewees called the new hybrid plans “a net positive for affected employees, especially teachers who may not spend an entire career in the government but will be able to access retirement benefits after a shorter tenure.”)

Read the full report here.

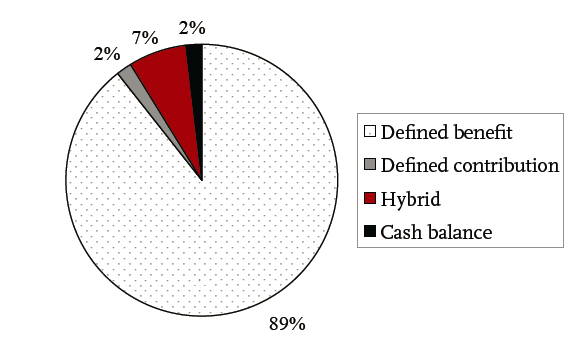

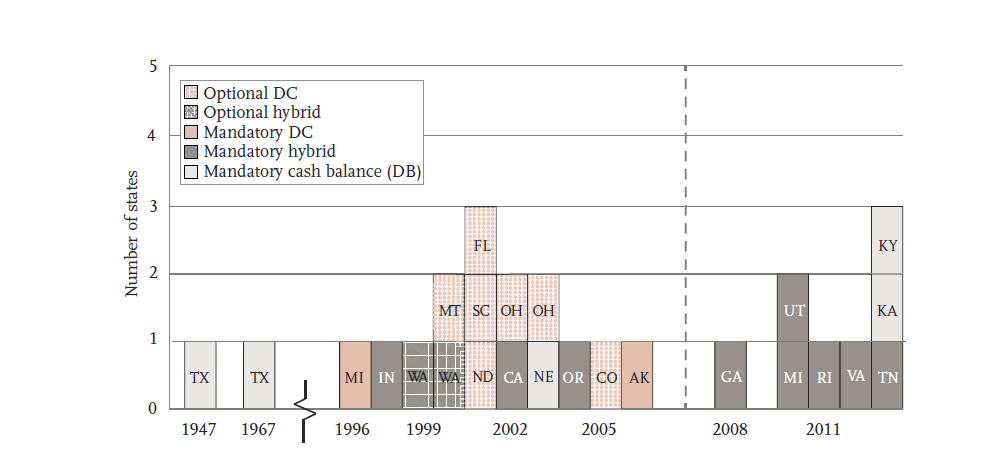

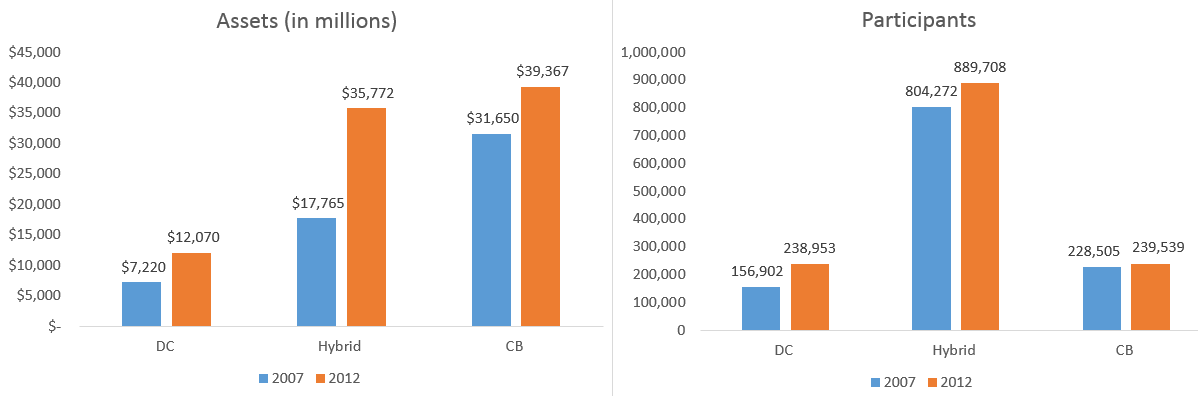

- There is a fear that defined contribution, 401k-style retirement plans will replace current state pension systems. While private sector employers now predominantly offer 401k plans, a recent Center for Retirement Research (CRR) report tracks the emergence of defined contribution plans and other options in the public sector. The authors find that few states have adopted pure defined contribution plans, but there has been a recent increase in the number of non-traditional retirement plans, including hybrid plans that combine less-generous defined benefit components accompanied by a defined contribution plan. These plans give employees greater money management options while reducing state financial burdens.Most states retain a traditional defined benefit (DB) plan for their public sector workers. These plans offer retirement benefits set by a pre-determined formula based on service years, final average salary, and a multiplier (i.e.: the benefit is “defined”). Currently 89 percent of state and local workers have a DB plan. On the other hand, only 2 percent of state and local workers have only a defined contribution (DC) plan, or plans in which employers and employees contribute set amounts but the end benefit remains unknown (i.e.: the contribution is “defined”).Distribution of State and Local Participants by Plan Type, 2012Source: Center for Retirement Research; Actuarial and financial reports; and Public Plans Database (2012).A small but growing contingent (about 11 percent) of public sector workers are enrolled in non-traditional plans including hybrid plans with DB and DC components, or another alternative plan called a cash balance plan. Cash balance (CB) plans are a type of defined benefit plan that sets an employee’s retirement benefit in terms of a stated account balance; at retirement, employees can choose whether they receive monthly payments or take their entire balance as a lump sum. Unlike traditional DB plans, CB plans increase the likelihood of making required contributions and therefore avoid large unfunded liabilities. Additionally, CB plans spread benefits more evenly between employees and therefore avoid the “back-loading” problem of traditional DB plans and are also portable.The chart below shows the adoption of defined contribution, hybrid, or cash balance retirement plans in their states through the years.Source: Center for Retirement Research; actuarial reports; state websites; National Association of State Retirement Administrators (2013); and Munnell (2012).As seen in the above bar chart, alternative retirement plans were virtually non-existent in the public sector except in one state (Texas) prior to the 1990s. Beginning in the mid-1990s, however, a number of states began to enact non-traditional retirement plans. From 1999 to 2004, six states created optional defined contribution plans: Montana, Florida, South Carolina, North Dakota, Ohio, and Colorado. These state plans gave public employees the option to enroll in a 401k style retirement plan. After the financial crisis in 2008, six states adopted mandatory hybrid plans: Georgia, Utah, Michigan, Rhode Island, Virginia, and Tennessee. Each of these plans included DB and DC components, usually with a smaller DB and a 401k-style DC with matching employer contributions. Two states, Kansas and Kentucky, created mandatory CB plans in 2013 that will begin enrolling new workers in the coming years.Nationwide over the last five years, the number of public sector workers enrolled in voluntary or mandatory defined contribution, cash balance, and hybrid plans combined climbed from 942,000 to over 1.1 million participants, while assets in those plans rose from a $22.9 billion to $46.6 billion. Hybrid plans alone grew from around 13.3 billion in assets to 21.9 billion from 2007 to 2012, and now have over 736,000 participants.The following charts show the growth in total assets and participants in DC, hybrid, and CB plans over the past 5 years.Source: Center for Retirement Research Appendix B. Assumes most recent year's assets data (2011) for Texas Muncipal TMRS.While the majority of states retain a traditional defined benefit system, a rapidly growing cluster of states have enacted alternative plans that offer greater career flexibility to individual teachers and greater financial sustainability for state and district budgets. This trend will likely continue in the coming years.

New York City Mayor Bill de Blasio has reached an agreement with the city's teacher's union on a new contract granting $3.4 billion in back pay. Here are three quick things to remember as the details continue to emerge:

1. As I noted on Twitter, the $3.4 billion in back pay is equivalent to about 1/8th of the teacher pension plan's $24.9 billion unfunded liability. All public policy decisions reflect a set of choices, and Mayor de Blasio and teachers union head Michael Mulgrew have just decided they value retroactive pay over the security of the city's pension plan. This doesn't even include the fact that higher salaries today will lead to higher pension payments every year going forward. Teachers nearing retirement will get an especially sweet deal because they'll have fewer years to pay into the pension system based on their new, higher salaries but many years to collect their enlarged pensions.

2. As a side note, I've seen numerous media accounts include a statement similar to one the Times ran, saying New York City teachers have "worked for nearly five years without a contract." That's not an accurate characterization. New York City teachers and schools were still bound by the rules in the old contract, and teachers were still paid according to the salary schedule ratified under the old contrct. There was no new contract, but that doesn't mean they didn't have a contract in place.

3. Even under the old, expired contract, indiviual teachers still earned raises. Teachers still progressed along the step-and-lane salary schedule. See the bottom of this post for an explanation from Chicago of how this plays out for individual teachers. In New York, a beginning teacher with only a bachelor's degree in 2008-9, the last year of the old contract, earned $45,530 in her first year. She would have earned $64,006 this year, an increase of 40.5 percent. A mid-career teacher with a Master's degree and 15 years of exerience would have earned $79,531 in 2008-9. This year, as a 20-year veteran, she would have earned $89,307, an increase of 12.3 percent.

Taxonomy:Today, employment and civil rights laws protect employees against discrimination--including age. Few probably realize, however, that states used to have laws specifically discriminating against the elderly. In New York, teachers were subject to mandatory retirement laws that capped the age a teacher could work. Thankfully, mandatory retirement laws do not exist anymore, but current pension systems do subtly encourage older teachers to retire.

According to a 1917 New York state law, teachers had to retire from the classroom upon turning 70 years:

“Each and every contributor who has attained or shall attain the age of seventy years shall be retired by the retirement board for service forthwith or at the end of the school term in which said age of seventy years is attained.” (New York State Laws, Chapter 18, Title 1, Section K, subdivision 2, 1917).

The law was mirrored in school policy. A 1921 high school handbook for New York City public schools teacher states: “Compulsory service retirement takes place at the age of 70, or at the end of the term in which the age of 70 is attained.” Regardless of the teacher’s performance or individual desire, a teacher in New York was forced to leave the classroom the year she reached age 70.

Even up until the 1960s and 1970s, mandatory retirement was a prevalent practice amongst private and public pension plans. A 1963 Department of Labor survey found that 67 percent of pension plans included some type of compulsory retirement. The original passage of the Age Discrimination in Employment Act of 1967 (ADEA) protected employees against age discrimination but limited protection to workers between the ages of 40 and 65 and allowed employer benefit plans to include mandatory age limits. A 1972 survey conducted by the Social Security Administration found that 58 percent of private and public pension plans still included some type of compulsory retirement. Congress later repealed the upper-age limit and only a few professions with intense physical requirements presently retain mandatory retirement (i.e.: police, fire fighters, air traffic controllers).

Today, the normal retirement age (the age when a teacher can begin receiving an unreduced pension benefit) in New York and New York City is age 63. Although mandatory retirement no longer exists, the current pension system has found other ways to subtly push older teachers out of the classroom. That is, by reducing pension wealth. The current pension structure “pushes” teachers out of the system by decreasing pension wealth for every additional year a teacher chooses to stay in the classroom beyond normal retirement. Once a teacher reaches the normal retirement age, every year she keeps teaching is a year she can’t receive her pension. Teachers nearing normal retirement consistently respond to this disincentive and leave the classroom because of the pension system.

Some may argue that these mechanisms are necessary to ensure an effective teaching workforce. Yet, the current policies are not tied to performance and may go against the desire of the individual teacher or school. Work disincentives are a blunt instrument based on age, not effectiveness. Policymakers trying to improve the quality of the teaching pool should consider using measures actually indicative of performance rather than age.

Randi Weingarten, the President of the American Federation of Teachers, used her most recent paid advertisement in The New York Times to dismiss any concerns about teacher pension plans. Weingarten is right to call out state policymakers for their fecklessness about properly funding teacher pension plans, part of the cause of the pension mess today.

But she then attempts to persuade readers not to worry about public sector pensions and instead focus on the retirement savings problems in the private sector. There are problems with private sector retirement savings--which we're worried about too--but that shouldn't prevent us from having a conversation about whether public sector benefits are meeting the needs of the workforce.

It's pretty clear that beyond the fiscal problems pensions are facing in some states, they also have design issues in an era of greater career mobility. Traditional teacher pensions work well for the small minority of teachers who teach in one place for their entire career but not for the majority of teachers who don't. So it's disappointing that Weingarten did not use this opportunity to call for retirement security for all public school teachers, our largest group of college-educated, middle-class workers.

Poorly structured retirement policies are actively hampering the retirement security of teachers:

- States and districts haven't saved enough money to properly fund pensions, and now they owe $390 billion more than they've set aside. Some states are making things even worse by failing to live up to their annual funding obligations, while other states have rapidly increased employee and employer contribution rates that are crowding out other school spending.

- Rather than creating a retirement system suitable for the mobile teaching profession, states have instead made it harder to earn a pension by increasing their "vesting periods." Approximately half of all Americans who begin teaching in public schools won’t qualify for even a minimal pension benefit because it takes so long to earn one--it takes a full decade in 17 states. By reducing the number of teachers eligible for a pension at all, states have trimmed their financial liabilities. That may make sense financially for the state, but it means fewer of Weingarten's members will leave teaching with a secure foothold on retirement saving.

- States have also built in specific barriers to mobility that restrict teachers from accessing employer contributions or interest on their own contributions. These savings penalties can add up to six figures for some teachers.

- Fifteen states prohibit teachers from enrolling in Social Security, forcing them to rely only on the state pension plan for their retirement benefits. Social Security can't replace teacher pensions but it should be one leg of a successful--and portable--retirement stool for teachers.

Rather than cast aspersions and demagogue the issue, teachers need leaders willing to have courageous conversations about how to modernize and improve retirement security for all of our nation's teachers.

Taxonomy: