The Baltimore Sun posted an article yesterday looking into why Baltimore County teachers are leaving in higher numbers this year compared to last year. It quotes a teacher, the school system’s chief human resources officer, and the vice president of the Maryland State Education Association all speculating on why. It could be new teacher evaluations. It could be what the article calls the “flawed rollout” of new curriculum tied to the Common Core. Or it could be a change in benefits allowing teachers who retire earlier to pay less in health care costs.

Or it could be just statistical noise.

First, as the article buries somewhat, teacher retirements or resignations are actually down across the region. I put the Sun’s numbers in the table below to illustrate the regional totals. Overall, there have been 584 fewer departures this year than last, a decline of 24.1 percent. Baltimore County itself has 57 more departures than it did last year (an increase of 8.6 percent), but that still represents less than 10 percent of Baltimore County’s teacher workforce.

School System

Number of Teachers Retiring or Resigning in 2013

Number of Teachers Retiring or Resigning in 2014

Anne Arundel

973

541

Baltimore City

157

173

Baltimore County

664

721

Carroll

174

103

Harford

221

159

Howard

235

143

Total

2,424

1,840

Second, new teacher evaluations, the Common Core, and the change in health care benefits are all statewide policies. None of these things are unique to Baltimore County, so it’s hard to believe they are responsible for its minor increase in teacher departures. Even if you believed Baltimore County’s rollout of new teacher evaluations and the Common Core were uniquely bad, you’re still stuck with the fact that these dramatic changes have led to a grand total of 57 additional departures. In a school system with 8,792 teachers, we’re talking about .006 percent of the district’s teaching workforce.

Ultimately, there are a number of factors that may affect teacher retention in any given year. We should be wary about trying to pin down any one reason, and we should be especially skeptical of narratives that try to explain small differences in a grand fashion.

Taxonomy:The Keystone Research Center (KRC), a Pennsylvania-based policy and budget organization, is out with a new brief analyzing pension reform proposals in Pennsylvania. Three quick thoughts:

- Their analysis is extremely incomplete. The brief provides examples of the pension reform’s effects on a narrow subset of workers—those acquiring at least 20 to 40 years of experience—but it never talks about what would happen to employees who stay less time. That’s a fatal flaw, at least in the case of teachers, because Pennsylvania’s pension system assumes more than three out of four Pennsylvania teachers leave within 10 years, let alone 20! The Keystone brief never mentions these people, but any serious analysis of pension reforms should include the effects on the vast majority of workers.

- When a pension analysis only focuses on 25- or 40-year veterans, it ignores what happens to those who will only accumulate a modest amount of service time. Pennsylvania currently requires teachers to stay for at least 10 years in order to qualify for a minimum pension benefit. Three-quarters won’t make it; they’ll leave their service in Pennsylvania public schools with no employer-provided retirement benefit. In contrast, the pension reform under consideration would place teachers in a hybrid pension/401k-style plan that offered employees their employer's contributions at the end of three years. The KRC analysis doesn’t include this among its list of benefits.

- Bizarrely, the brief presents potential salary increases as a bad thing. It identifies “hidden wage increases” as a cost because employers may respond to lower pension contributions with higher salaries. Because wages are subject to federal income tax whereas pension contributions are not, the brief says pensions are a “less efficient tool for improving retention.” This is crazy talk. First, consider the counter-factual: If an employer decided to compensate an employee entirely through a pension system, it would be more efficient from tax purposes, but it would mean the employee had zero cash to spend on rent, food, or any other living expenses. At some point there’s a tipping point where tax “efficiency” is no longer as important. Second, the entire concept of efficiency is moot if workers don’t value what comes out of it. Most workers are aware of and appreciate the flexibility of $1 in cash far more than $1 in benefits. In Pennsylvania, employer contributions currently sit at 16 percent of teacher salaries but could potentially rise as high as 20 or 30 percent in the near future. Teachers may actually prefer to have the cash.

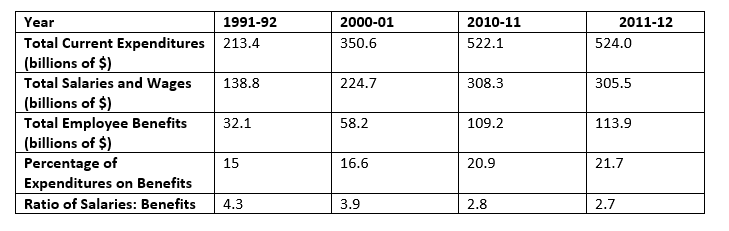

The Census Bureau’s latest Public Education Finances Report is out, and it shows that employee benefits continue to take on a rising share of district expenditures.

The table below uses 20 years of data (all years that are available online) to show total current expenditures (i.e. it excludes capital costs and debt), expenditures on base salaries and wages, and expenditures on benefits like retirement coverage, health insurance, tuition reimbursements, and unemployment compensation. Although it would be interesting to sort out which of these benefits have increased the most, the data don’t allow us to draw those granular conclusions. But they do tell us that teachers and district employees are forgoing wage increases on behalf of benefit enhancements.

From 2001 to 2012 alone, public education spending increased 49 percent, but, while salaries and wages increased 36 percent, employee benefits increased 96 percent. Twenty years ago, districts spent more than four dollars in wages to every one dollar they spent on benefits. Now that ratio has dropped under three-to-one. Benefits now eat up more than 20 percent of district budgets, or $2,363 per student, and those numbers are climbing.

This is not a good trend. Instead of hiring more teachers or paying them more money, districts are devoting an increasing share of finite resources to employee benefits.

Taxonomy:In our recent paper "Friends without Benefits," we used pension plan assumptions for all 50 states and the District of Columbia to estimate that more than half of all teachers won't qualify for even a minimal pension. They'll leave the teaching profession without a retirement benefit at all. Those figures are shocking, but a new report suggests our estimates may actually be too low.

We focused on the question of whether teachers "vest" into their pension plan because it's an important milestone for workers and determines whether they'll qualify for at least a minimal pension when they retire. States set a vesting period, broadcast it to workers, and guarantee at least some retirement income to those who who meet it. Workers can be confident the pension will be there for them in retirement and increase with inflation as they age. That's a nice protection, but reaching the minimum vesting requirement guarantees only a minimum annuity in retirement.

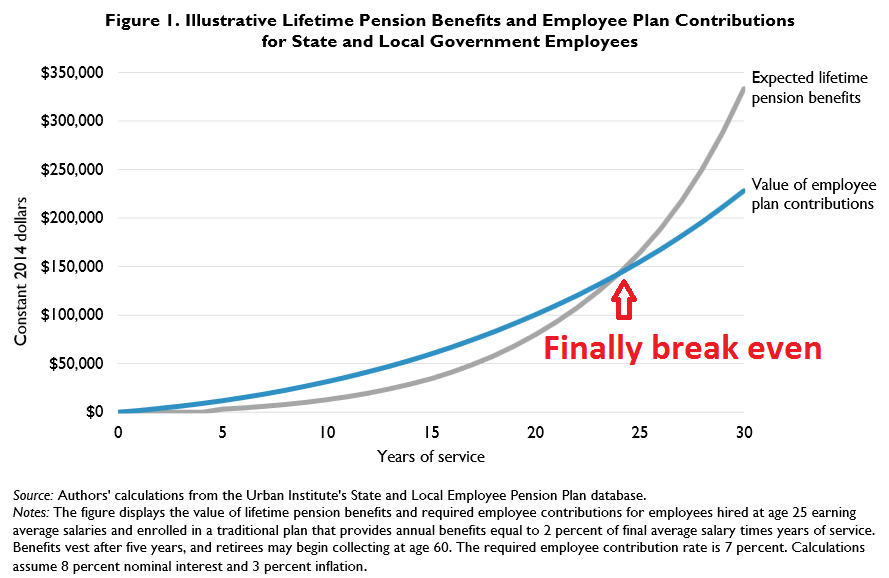

A new Urban Institute brief suggests vesting isn't nearly sufficient. In fact, the vast majority of teachers will leave the profession with less than their own contributions. Figure 1 from the Urban brief (reproduced below) shows an illustrative example of how this works. It looks at a 25-year-old beginning their employment under a hypothethetical (but typical) pension plan. The plan provides an annual pension equal to 2 percent of the worker's final average salary multiplied by years of service. The chart assumes an employee contribution rate of 7 percent, an 8 percent investment return, and a 3 percent inflation rate. The employee vests at five years, at which point they're guaranteed at least some level of pension when they reach age 60, but the minimum pension is not worth very much.

The blue line shows the value of the employee's own contributions and the gray line shows the value of the pension. As you can see, the gray pension line rises above $0 after the employee vests at year 5, but the pension doesn't surpass the employee's contributions until the employee has accumulated nearly 25 years of service. At that point, the value of the pension skyrockets well above the employee's own contributions.

This is merely an illustrative example, but Urban has run the calculations to find the break-even point for every large state pension plan. In the median state, teachers must wait 24 years (!) before their pension is finally worth more than their own contributions.

To put it mildly, this is a long time. Many teachers leave the profession or cross state lines after only a few years, let alone staying put for much longer. Based on our calculations from state pension plan assumptions, the median state assumes that only 23 percent of teachers will stay for at least 24 years.

These calculations are dependent on each plan's particular rules and assumptions, and the chart above relies on an 8 percent investment assumption. That may seem high, but it closely mirrors typical state pension plan assumptions. Besides, Urban has run similar calculations with lower assumed rates of return and still placed the break-even point at about 15 years (see Figure 1 here). Because teachers have such high attrition rates in the early years of their career, the median state assumes that more than 70 of teachers will be gone before even this lower break-even point. The rest will leave the profession with no pension at all, or a pension worth less than their own contributions.

Unfortunately, states have been making their pension plans less and less generous to new teachers: They've made their pension plans less generous for full-career workers, and they've lengthened vesting requirements, making it harder to qualify for a pension at all. And the Urban Institute's calculations show that states that made changes to their pension plans in response to the recent recession raised the number of years it takes for an employee to break even from 20 to 24 years. These long time delays are penalizing hundreds of thousands of teachers all across the country.

When a teacher leaves, she has the option of taking her retirement contributions with her or leaving them in the system. Most pension plans assume that 100 percent of teachers who do not qualify for a pension who leave the system will take their contributions with them (even though this is not always the case). But for a teacher who does qualify for a pension (a vested teacher), the odds of her taking her contributions as an immediate cash payment or waiting for a pension upon retirement are a bit more mixed.

We searched public pension plan documents to find what happens to departing teacher contributions. Do they roll over their funds into another retirement account? Do they cash the money out and use it for something else (called “leakage”)? We ultimately failed to find this type of information--plans don't track what happens after teachers leave them--but we did find some data on how frequently vested teachers cash out. From our scan of state pension documents we found that:

- The District of Columbia Retirement Board (DCRB) assumes 35 percent vested teachers who leave will withdraw their contributions.

- California State Teacher Retirement System (CalSTRS) assumes 29-34 percent of vested female teachers with 10 years of service will withdraw their contributions, depending on their age.

- Idaho Public Employees Retirement System (IPERS) assumes 6 percent of 25-year-old vested females who leave will withdraw their contributions, and 15 percent of 45-year-old vested female who leave will withdraw their contributions. Idaho's assumptions include teachers and other public sector workers.

Additionally, all plans itemize the total dollar amount of their refunds. CalSTRS reported over $100 million in refunded contributions to departing teachers. Compare this to the amount spent on the cost of administering CalSTRS ($139 million) and the system’s total benefits payments ($11 billion). The District of Columbia reported $5.3 million in refunds to teachers. Virginia reported 8,530 withdrawals totaling $81.5 million to teachers and other public sector workers (or an average of $9,555 per worker). Kansas reported 9,500 withdrawals totaling $48 million to teachers and other public sector workers (or an average of $5,052 per worker). Many of these withdrawals are considerably smaller than they would be in the private sector or if teachers had access to their employer's contributions.

These data points indicate that there are teachers who are eligible for a pension but, for whatever reason, choose not to take it. Pension plans don’t track what happens to withdrawn contributions, so we don’t know exactly why these teachers are choosing to forgo their pensions. They could be cashing out the funds for personal use or rolling over the funds to another retirement account. If teachers are choosing to cash out, however, they will face costly “leakage” tax penalties for withdrawing funds for non-retirement purposes (a growing problem in the private sector). Ideally, it would be useful to know the percentage of non-vested who leave their contributions behind. Pension plans, however, usually assume that all non-vested teachers take their contributions and only report the likelihood that vested teachers withdraw contributions. Pension plans could guide individual teachers through their choices and how they could best maximize their retirement savings.

Last week I presented our work on teacher pensions at the Education Writer’s Association (EWA) 67th national seminar. Education Week’s Stephen Sawchuk moderated the panel featuring Richard Ingersoll from the University of Pennsylvania, Susan Headden from the Carnegie Foundation for the Advancement of Teaching, and me.

Richard discussed his newly updated report on seven key trends affecting the teaching workforce, including the trends of teachers becoming more mobile and far less experienced than they were a generation ago. Susan discussed her recent report on what changing teacher demographics means for schools, students, and society. I focused on what this trend means for individual teachers and their retirement savings:

Why do pensions belong in this discussion? To begin with, pensions are an excellent source of local data. While Richard’s work presents a national picture of the teaching profession, the only place to find regular, high-quality data on state or local teacher retention data is the pension system. Pension plans keep detailed records of who stays and for how long, where they work, and how much money they earn. In order to estimate how much money it will need to pay in future benefits, pension plans also have to project future retention rates. Pensions publish those “withdrawal” estimates tailored to years of experience, age, and gender. Because these withdrawal assumptions are tied to large financial decisions, pension plans conduct regular “experience studies” to check their assumptions and compare their expectations with actual teacher turnover rates.

Every pension plan makes these calculations. They’re often buried in technical “comprehensive annual financial reports” under the terms “withdrawal” or “termination” assumptions. But they can tell us a lot about each state’s teacher workforce. For example, in Illinois we can see the state estimates that 10 percent of its “non-vested” 40-year-old female teachers (those with fewer than 10 years of experience) will terminate their employment in the next year. We can use the same table to create longer-term retention rates.

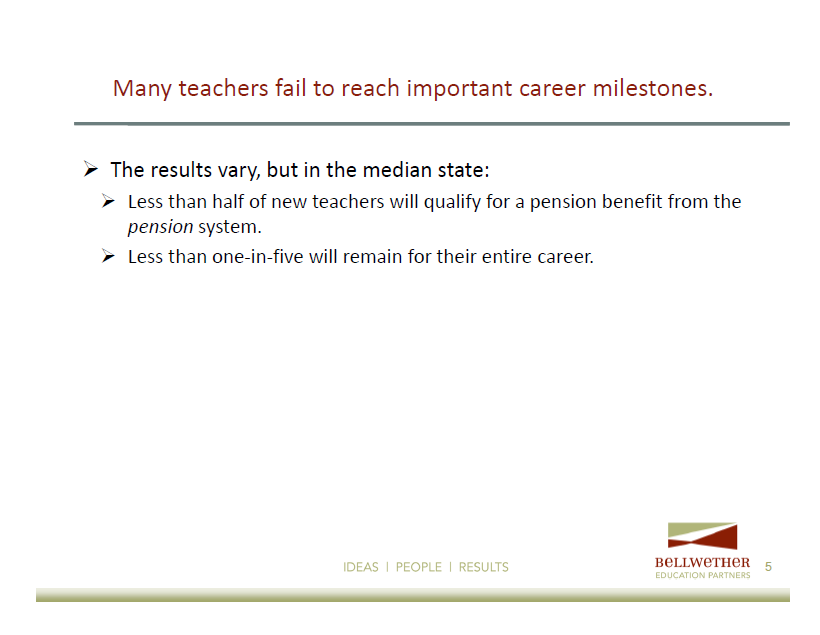

It's possible to use these retention rates to estimate what percentage of teachers in each state will reach various career milestones. In particular, as states have created longer "vesting periods," the time teachers must work before qualifying for a minimum pension, they're offering retirement benefits to a smaller and smaller share of today's teachers. Nationally, nearly half of all new teachers leave within 5 years. That's exactly where half the states have set their vesting requirements, although 17 states now require teachers to remain at least 10 years.

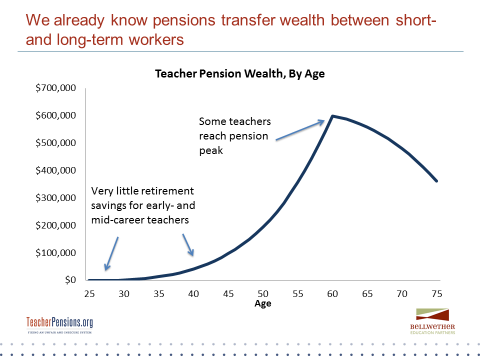

The result is that many teachers will fail to vest and will leave their years of service without a pension. In the median state, less than half of teachers will stay long enough to qualify for even a minimal pension.

Unfortunately, pension systems are designed for a much more stable workforce. Only a small fraction of teachers will remain a full career and earn a relatively comfortable pension. In the median state, less than one-in-five teachers will stay long enough to realize the benefits that begin accruing at the back-end of teacher careers. The majority of teachers will receive very little in the way of retirement savings.

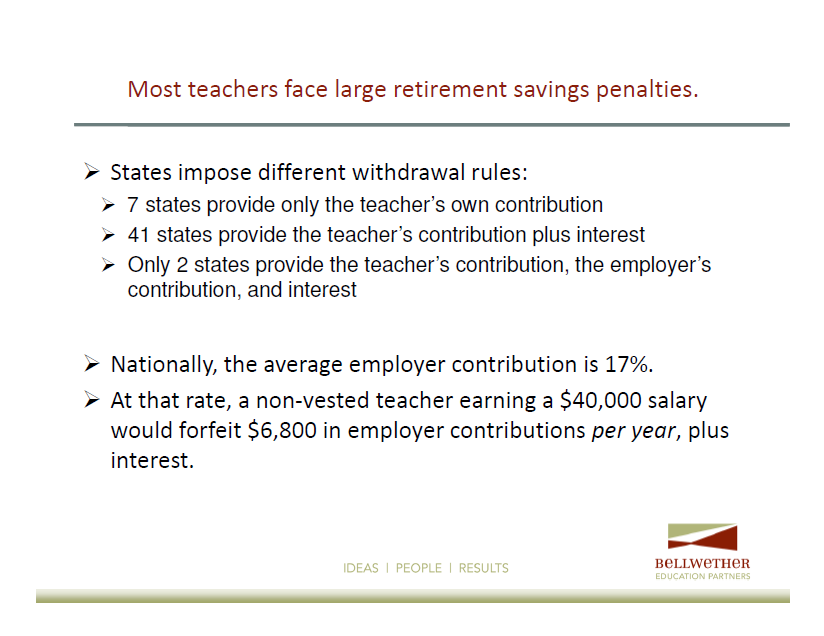

States impose their own rules on teachers who leave before vesting and want to withdraw their contributions. In seven states teachers are eligible for only their own contributions. 41 states provide teachers with their own contributions plus some interest on those investments. But only 2 states provide the teacher their own contributions, some interest, and a share of the contribution employers made on their behalf. Nationally, the average employer contribution rate is 17 percent. That's technically part of teacher compensation, but a teacher who leaves before qualifying for a pension forfeits those contributions. The money stays with the pension plan and can be used to supplement the pensions of those who remain. Meanwhile, individual teachers forfeit thousands of dollars in retirement savings.

We'll continue to follow teacher retention and retirement trends here are TeacherPensions.org. Please check back for more information as we continue to write and blog about the issue.