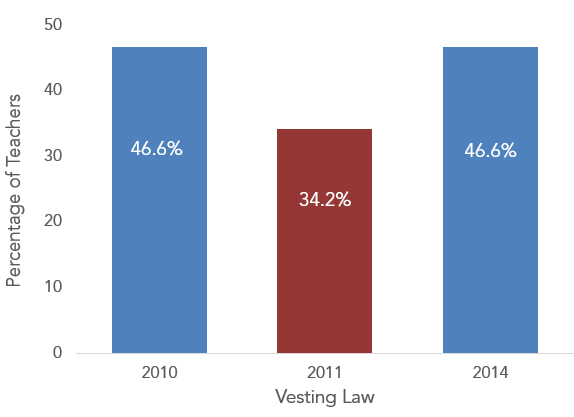

- North Carolina recently passed legislation that will make it easier for teachers to receive retirement benefits. The new law lowers the minimum service requirements (aka the “vesting requirement”) teachers need to qualify for a pension from 10 years to 5 years, in addition to giving contribution interest to unvested teachers.Teachers who teach for at least 5 years are now eligible for a pension annuity when they retire. And teachers who teach less than 5 years will receive 4 percent interest on their own, refunded contributions (they still do not receive any portion of the 14.69 percent employer contribution). Originally, teachers who did not meet service requirements could only receive a refund of their contributions without interest; only fired teachers who did not meet service requirements could receive interest on their contributions.Under the new law, more teachers will be able to receive basic retirement benefits. According to state pension plan assumptions, only 34 percent of teachers would have qualified for a pension under the old law. Now, an estimated 47 percent of teachers will qualify for a pension under the new law. This means that an estimated 12 percent (or around 11,000) more teachers will vest and qualify for a basic pension, as opposed to nothing. Although more than half of North Carolina's teachers still will not remain long enough to qualify for a minimum pension, they will at least receive 4 percent interest on their refunded contributions.

Teachers Who Are Eligible for Pension Benefits

*Based on withdrawal assumptions found in the 2010 - 2014 North Carolina Comprehensive Annual Financial Reports.Like many other states, North Carolina previously increased service requirements in 2011. North Carolina legislators believed that it could lower costs by increasing its service requirements, essentially making it more difficult for teachers to receive a minimum pension. However, the state treasury stated that the harsher requirements did not have significant cost savings. The treasury contended that the 2011 law was additionally too strict and not in line with other public and private sector plans:“A decade is too long for teachers and state employees to have to wait to be vested in their retirement system. By restoring the 5-Year vesting period, this legislation allows the state of North Carolina to be more competitive as an employer relative to other public and private retirement benefits.”Recently, the legislature also passed a budget that will raise early career teacher pay by an average of 7 percent for teachers with 1 to 4 years of experience and up to 18.5 percent for teachers with 5 years of experience.North Carolina legislators deserve credit for reversing course and enhancing the retirement security of the state’s teachers. A 2012 California law reduced pensions for new members and attempted to limit the ways employees could artificially "spike" their pensions by cashing out unused sick or vacation leave or taking on overtime in their last years of employment. Because pensions are based on a formula reflecting an employee's final average salary, employees can receive lifetime pension benefits by inflating their compensation in their last years of employment. In implementing the law, the California Public Employees’ Retirement System (CalPERS) recently announced 99 different types of compensation they consider "pensionable." Governor Jerry Brown, a strong advocate for the 2012 law, is looking into possible recources of action, but in the meantime here are some of my favorites from the list:

- Dictation/Shorthand/Typing Premium - Compensation to clerical employees for shorthand, dictation or typing at a specified speed.

- Longevity Pay - Additional compensation to employees who have been with an employer, or in a specified job classification, for a certain minimum period of time exceeding five years.

- Physical Fitness Program - Compensation to local safety members, school security officers and California Highway Patrol officers who meet an established physical fitness criterion.

- Audio Visual Premium - Compensation to miscellaneous employees who are routinely and consistently responsible for operating audio visual equipment.

- D.A.R.E. Premium - Compensation to local police officers, county peace officers and school police or security officers who routinely and consistently provide training to students on drug abuse resistance.

- Confidential Premium - Compensation to rank and file employees who are routinely and consistently assigned to sensitive positions requiring trust and discretion.

- Parking Citation Premium - Compensation to employees who are routinely and consistently assigned to read parking meters and cite drivers who have violated parking laws.

- Traffic Detail Premium - Compensation to employees who are routinely and consistently assigned to direct traffic.

- School Yard Premium - Compensation to part-time school district employees who are routinely and consistently assigned to supervise students during recreation.

There's also there's a premium for firefighters assigned administrative work during regular hours (as opposed to actually putting out fires) and a premium for employees who routinely deal with sprinklers. Under the new CalPERS rule, employees may have to deal with sprinklers while they're employed, but the state will compensate them with a pension "sprinkler premium" for the rest of their lives. Read the full list here.

Taxonomy:The U.S. Department of Education recently released the results from the 2012-13 principal staffing survey. Like the survey on teachers, principals were tracked as “stayers,” “movers,” and “leavers,” where stayers are principals who remain in the same school, movers are principals who transfer to another school, and leavers are principals who leave the profession either to retire or go elsewhere. The survey also breaks down the data across various groups, such as traditional public schools and charter schools and principal demographics.

- Compared to teachers, a slightly lower percentage of principals stayed in their schools. While 81.4 percent of public school teachers remained in the same school the following year, only 79.5 percent of public school principals stayed put. Principals also had a slightly higher likelihood of completely leaving the profession than teachers, who were slightly more likely to move between schools.

- Most principals have very little experience. Almost three-quarters (73 percent) of principals have less than 5 years at their current school (as of 2011-12), and about half (49 percent) of all principals have less than 5 years at any school.

- Most principals were teachers before becoming a principal. 60 percent of all public school principals had 10 or more years of teaching experience before becoming a principal, and 90 percent had 5 or more years of experience.

- There were some turnover differences between principals at traditional public schools and charter schools, but the discrepancy is not as large as some may think. Principals at public charter schools have slightly lower retention rates (71.2 percent) than principals at traditional public schools (77.8 percent). 11.4 percent of principals at traditional public schools left the profession, compared to 12.2 percent of principals at public charters.

- As with teachers (and many non-education professions) principal turnover was lower during the recent recession. In 2012-13, 77.4 percent of public school principals stayed in their schools; this percentage is a slight decrease from the 79.5 percent reported in the 2008-09 survey.

The new report has several implications for pensions. Public school principals, administrators, and teachers all participate in the same pension plan. Most plans continue to use a traditional defined benefit formula which calculates pension wealth by multiplying an employee’s years of service by final average salary and a multiplier. When a teacher becomes a principal, she does not give up her pension so long as she remains in the same retirement system. But principals have substantially higher salaries than teachers, and these salaries in combination with a full career in a single retirement system (which can include teaching years), result in lucrative pensions. In Missouri, a teacher who stays for a full career accrues $250,000 in pension wealth, while a principal accrues over $360,000 in pension wealth for a full career.

According to the new staffing survey, 60 percent of public school principals had 10 or more years of teaching experience. This is a good thing for a principal’s ability to lead a school, but makes his or her pension much more expensive because years spent teaching count toward pension benefit formulas. As with teachers, traditional defined benefit plans create strong incentives for administrators nearing normal retirement to continue on the job until their pension wealth peaks, and the turnover rates from the principal survey confirm this trend. Pension wealth is even more backloaded for school leaders because their salaries are higher than teachers and pension formulas only take into account ending rather than starting salaries.

As suggested by a recent Fordham report, districts should consider paying principals more to attract strong candidates. Rather than paying principals substantial retirements at the back end, districts can pay more upfront in salary.

Taxonomy:We often write about statistics or theoretical arguments about teacher pensions. But pensions aren’t just some technical policy that exists in a vacuum—they affect the lives of millions of teachers. We’ll be doing an occasional series chronicling those stories and how pensions affect individual teachers and former teachers.

Before working for Bellwether, I worked as a teacher in Maryland. I wanted to make a difference for students, especially those who were socioeconomically disadvantaged. Pay and benefits were of course necessary for a comfortable living but were, overall, only a peripheral concern.

During our new teacher induction, I signed multiple forms including a contract stating that I would contribute to the Maryland State Retirement System. I saw that 5 percent (later increased to 7 percent) was deducted from each of my paychecks to the state. I presumed that these contributions would go toward a safe nest egg that I could later claim and possibly even get for the rest of my life, or at the very least, that my contributions would be mine to take wherever, just like my 403b savings from prior work. (Only later did I learn that pensions are not portable, and purchasing service credit is expensive and impractical in most cases.) I had a vague understanding that the state would take care of my contributions, so I didn’t need to worry about choosing what portfolio investment blend I wanted. Other than that, however, I wasn’t concerned with my retirement benefits and assumed that the state had my best interest in mind. There were so many other teaching responsibilities that I needed to take care of for my students and school.

Now, I know how the odds are stacked against most teachers. In Maryland, the state pension plan assumes that over half of new teachers (57 percent) will not remain long enough to qualify for a minimal pension. Like many other states facing budgetary pressures, the Maryland legislature increased the required number of years to qualify for a pension, making it even harder for teachers to receive basic retirement benefits. Maryland teachers who leave before meeting service requirements can withdraw their contributions plus a generous 7 percent interest, but do not receive any portion of the state’s contributions which currently are around 13 percent of payroll. Very few states allow teachers to withdraw any portion of their employer contributions before vesting, and teachers in certain states receive less than their own contributions. I was fortunate to get at least my contributions back plus interest, but can’t claim any portion of the $20,000 plus in employer contributions made over three years on my behalf.

I also know that, even for those who do meet service year requirements, teachers are severely shortchanged. A teacher who stays for 10, or even 20 years, may not come out ahead. According to a recent Urban Institute report, a teacher in the median state needs to teach a minimum of 24 years in the same state retirement system in order to simply break even on their own contributions. Many teachers contribute toward the system, while few actually make any net gain.

Teachers nearing retirement understand the weight and importance of a hard-earned pension. But retirement security is unfortunately a peripheral issue unless you are closely approaching it. Pension plan reports, while publicly available, are esoteric, and few early and mid-career teachers have the time to carefully examine and project their benefits over time to see the penalties. Moreover, most teachers will make personal life decisions—move to another state or switch to another sector—in spite of their pension. Rather than continuing systems that disadvantage the majority of teachers, states should consider plans that can provide secure and flexible retirement benefits for all teachers.

Taxonomy:A new report from the National Institute on Retirement Security (NIRS) claims that state, local, federal, and private pensions contribute $555 billion to the American economy's GDP. They write:

This is roughly the same amount of value added as was contributed by the entire construction industry, which generated $581.1 billion in value added in 2012.

Using the same methodology, NIRS could claim that pensions contribute more than three times as much value to the Gross Domestic Product as a category labeled "Agriculture, forestry, fishing, and hunting." To put it another way, NIRS is claiming that pensions contribute more economic value than the combined total of all air, rail, water, truck, transit, and pipeline transportation.

These comparisons should strike you as insane. Pensions are a savings and investment tool that transfer money from one class of people (workers) to another (retirees). Like Social Security, pensions may be large in terms of dollar amounts but their sheer size should not distract us. Although NIRS wants to double-count it, pension investments in the stock market are already reported in official GDP calculations when companies spend money building a plant or buying raw materials. Pensions themselves don't actually contribute to GDP. NIRS is a pension trade group so they have an incentive to suggest otherwise. But you don't have to take their claims at face value.

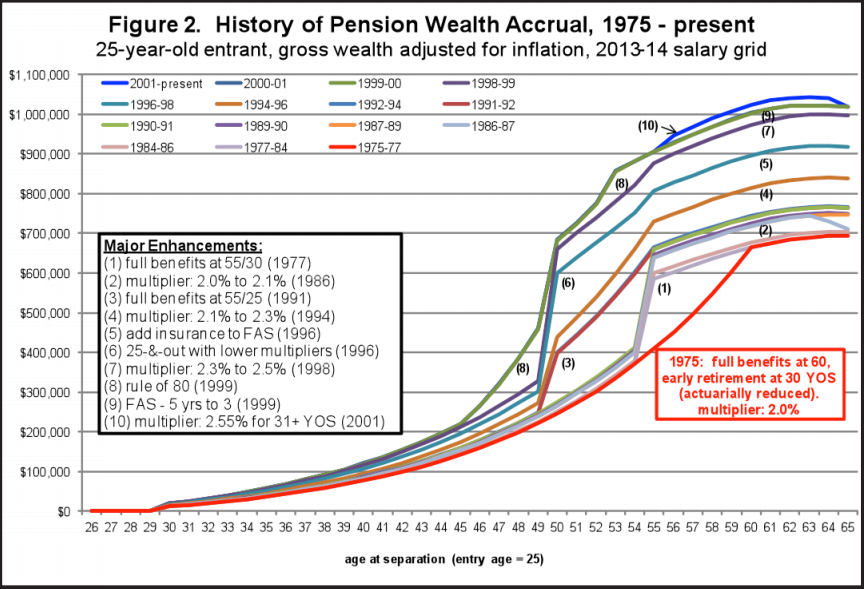

Taxonomy:The chart below may appear complicated, but it explains a lot about what’s happened over time to teacher pensions. It comes from a Show-Me Institute brief from Bob Costrell. Each line represents the pension wealth accrual (essentially a teacher’s annual pension multiplied by the number of years she can expect to receive it) for 25-year-old females at given points in time. The lines have been adjusted for inflation, and they use the current salary schedule for Jefferson City, Missouri.

The bottom line (in red) represents the pension plan offered to Missouri teachers in 1975. It was a fairly standard pension plan. Teachers did not qualify for any pension at all in their early years before “vesting” at five years, earned a relatively small pension for the next 10-15 years, and then accelerated toward a much higher peak at the back-end of their career. Back in 1975, that peak was at age 60 (it had been age 65 in 1967).

Over the years, and especially during the 1990s when the stock market was booming, legislators increased pension benefits significantly.* But they have not distributed those increases evenly to all teachers. There has been no change at all for teachers who serve for five years or less, which in Missouri is now about 42 percent of all teachers. And there have been comparatively small changes for Missouri teachers who serve for 15 or 20 years (about 2/3rds of the workforce).

The biggest changes have been near the back-end, for teachers with 25 or 30 years of experience. In inflation-adjusted terms, Missouri legislators have doubled or tripled the pensions of full-career teachers.

As the brief describes, these increases eventually came with a cost. Legislators raised teacher contributions to the pension plan from 8 percent of salary to 14.5 percent today. All Missouri teachers today pay those costs, even though the majority of them won’t benefit from the pension increases. In fact, a research paper earlier this year found that Missouri's higher contribution rates more than offset any gains a new teacher might make from the pension enhancements. If you want to know why districts can’t afford to give base salary increases to early- and mid-career teachers, these type of pension enhancements are a big reason why.

*Note that the increases were retroactive, meaning a teacher who started in 1975 but retired in 2005 received not what she was promised when she started but the much higher benefit passed before she retired.