The Consortium for Policy Research in Education (CPRE) released a report on the changing trends in the teaching workforce. Over the past decade, an increasing percentage of teachers have either moved to another school or left the profession altogether, and has only tapered slightly after the recession.

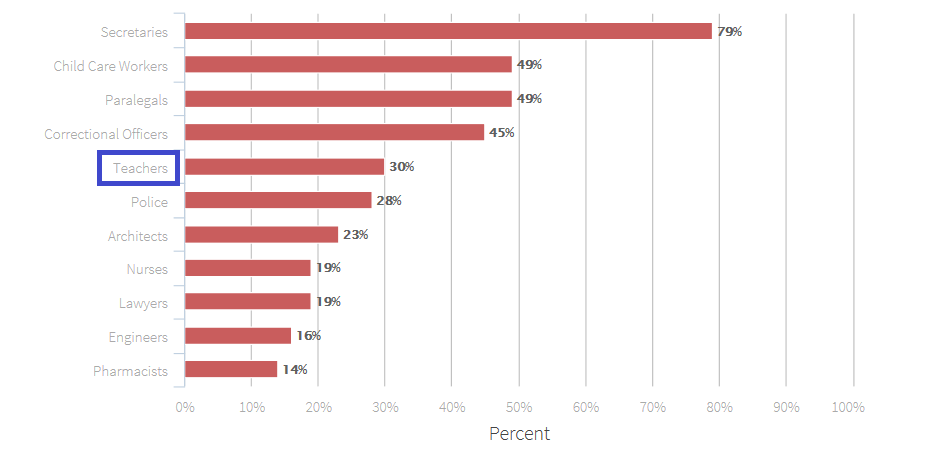

How does teacher attrition compare to other professions? The chart below shows the percentage of college graduates who entered a particular occupation (e.g., teaching, architecture, engineering, etc.) in 1997 but then left that occupation by 2003.

Employee Turnover By Occupation

Source: Ingersoll, R. & Perda, D. 2014. This chart originally appeared in the CT Mirror.

Of the college graduates who became teachers, 30 percent left within six years. Teachers leave the profession at about the same rate as police officers, while having double the attrition rates of engineers and pharmacists. On the other hand, teachers had significantly less turnover than secretaries, child care workers, and paralegals.

Compared to other occupations, teachers and police officers are among the few professions that still participate in a pension system. Pension systems are best suited for employees who stay an entire career, but they generally benefit only a small percentage of teachers because of high turnover in the profession.

Today, the Illinois Teacher Retirement System provides qualifying teachers with a defined benefit pension. Once a teacher reaches the required number of service years, she qualifies for a pension which increases over time as she accumulates years in the classroom and increases in her salary. A teacher with more years in the classroom (who receives a higher salary) will have a larger pension than one who served for less time (and receives a lower salary).

A hundred years ago, however, Illinois teachers received a fixed, annual benefit that was determined independent of salary: a “flat pension.” The first Illinois pension laws were passed in 1915, and stipulated that a teacher who taught for a minimum of 25 years and was at least 50 years old qualified for a flat $400 annual benefit:

“To service pensioners—annuity of $400 per annum is paid to a teacher who retires after the attainment of age fifty, having served in the public schools of the United States for at least twenty-five years, the last fifteen of which have been spent in the public schools of Illinois, and provided the teacher has paid the sum of $400 into the fund.”

As a 1918 Illinois legislative commission found, there were severe issues with the original pension system. A teacher’s pension amount remained preset at $400, regardless of her salary or whether she taught for more than the required twenty-five years. “Under the Illinois law, the pension is $400 per year, regardless of the salary.” Plus, in order to qualify for a benefit, teachers needed to serve a minimum of 25 years, a fairly high threshold. For context, around the same time New York City estimated that nearly half of its teachers would leave the system before reaching 25 years of service. (If Illinois were to apply the same 25-year requirement today, only 23 percent of teachers would qualify for a pension according to current assumptions.)

Making matters worse, an Illinois teacher in 1915 who left the system before serving 15 years would only get half of her own contributions. And teachers who taught between 15- 24 years would neither qualify for the flat $400 annual pension nor receive a refund of their own contributions.

"Under the Illinois system, the withdrawing employee receives one-half of the sum contributed, if the contributor ceases to teach before serving fifteen years, but he receives no refund if he withdraws after giving more than fifteen years of service."

Under this rule, a teacher who taught 15 years was worse off than a teacher who taught 14 years or less. With such strict longevity requirements, a teacher who taught anything less than twenty five years would lose out on a benefit and potentially all of her original contributions. Current pension systems are often described as having "push-pull" effects that keep teachers in until they reach a certain number of years of service or encourage them to leave once they reach prescribed milestones. The old Illinois system was even worse, and essentially pushed people out at 14 years or trapped them until they reached 25 years.

Illinois would continue operating under the original 1915 pension laws until 1939 when the modern-day Teacher Retirement System was created. In 1939, Illinois restructured the teacher’s pension system (which struggled to remain solvent) so that pensions were based on salaries and the minimum service requirement was reduced to 10 years. In 1941, the minimum service requirement was further reduced to 5 years. It stayed that way until 2011, when the pension fund was in such dire financial straits that the legislature increased the minimum service requirements back to 10 years to reduce costs at the expense of teachers.

Illinois has improved its teacher retirement benefits since 1915, but still has much to improve.

Pension debates often turn on traditional defined benefit versus 401k-style defined contribution plans. But in practice there are many more options to choose from. A new Manhattan Institute report by Josh McGee and Marcus Winters examines an alternative defined benefit plan. The authors (one of whom works at a foundation that funds some of Bellwether’s pension work) call the alternative plan a “smooth-accrual defined benefit plan” or SA-DB. In a traditional defined benefit plan, benefits are heavily backloaded; teachers receive minimal benefits in their early years but quickly earn substantial benefits as they near their plan’s prescribed “normal retirement age.”

In contrast to a traditional defined benefit plan, a SA-DB plan accumulates wealth at a constant rate. This means that early-career teachers, who usually gain little to no benefits from traditional plans, can receive more benefits from the start. The benefits of that approach, the authors argue, is that SA-DB plans wouldn’t necessitate higher taxes and could mean greater retirement security for more teachers.

The SA-DB plan is essentially what others have called a “cash balance” defined benefit plan. These plans allow teachers to earn a constant percentage of benefits; pension wealth is smooth and even, in comparison to the sharp, backloaded spikes in traditional plans. While there are only a few winners and a much larger pool of losers in the current system, a smooth accrual model would allow more teachers to gain secure, retirement benefits from the onset of their careers.

The Manhattan Institute report looks at which plan a teacher would prefer: a traditional defined benefit or a SA-DB plan? They use economic modeling and pension plan assumptions from 10 of the largest public school districts to predict what a risk-averse teacher would prefer. They find that:

- Newly entering teachers would prefer the less backloaded, SA-DB plan.

- How much an entering teacher prefers the SA-DB plan depends on how backloaded the competing traditional plan is and the how likely the teacher will stay in the plan. In most districts, newly entering teachers would have a strong preference for the SA-DB plan.

- Newly entering teachers working in heavily backloaded plans would rather get a small amount of money upfront than stay in their pension plan. For example, in Hawaii, a teacher is better off passing over her traditional plan in exchange for just $279 because plans are so heavily backloaded and turnover is high. According to current plan assumptions, most Hawaiian teachers (77 percent) won’t even earn $279 when they leave the system.

- Newly hired teachers in six districts who expect to stay for 10 years would also prefer the SA-DB plan.

- Teachers who expect to stay for 20 or more years would prefer the traditional plan. These teachers (a relatively small pool) are unlikely to leave the system because they are close to earning maximum pension benefits.

Most people consider rising teacher retention rates a good thing. Teachers tend to improve rapidly in their first few years on the job, so increasing retention rates means students may likely be getting better teachers. Financially, it costs school districts money to recruit and train new teachers, so an increase in retention rates would let them save on those costs (although they have to pay more experienced teachers hirer salaries).

But one poorly understood aspect of rising retention rates is that they also lead to rising pension costs.

In order to be eligible for a pension, teachers must meet a minimum number of employment years or a “vesting” requirement before they receive rights to a pension. As discussed in Bellwether's recent paper, 24 states and the District of Columbia have a vesting requirement of five years and another 17 states require a teacher to stay 10 years before qualifying for a pension. Those vesting periods are rising; in 2009, during the economic recession, 12 states increased their vesting periods. The increase in vesting period saves states money by making it more difficult for teachers to earn a pension. Bellwether's research suggests that only a small percentage of teachers will make it to their state vesting requirement. Fewer teachers earning a pension means lower costs for the pension plan and less retirement security for those affected teachers.

Illinois was one of the states that increased its vesting requirements. Before 2011, teachers were required to work at least five years to be eligible for a minimum pension. In 2011 Illinois increased the vesting period as part of a pension reform law to reduce the state’s unfunded pension liability. The law (Public Act 96-0889) created two tiers of teachers. Teachers in Tier 1, those who were employed before January 1, 2011, continue to vest after five years of services. Tier 2 teachers are those who entered employment on or after January 1, 2011. They must serve 10 years before reaching eligibility for a pension. Citing the Commission on Government Forecasting and Accountability, a synopsis of the bill notes that the change in retirement age combined with a pension salary cap will save the state $43.86 billion. The actuarial assumptions anticipated increases in teachers staying, and lawmakers responded with tougher retirement policies. *

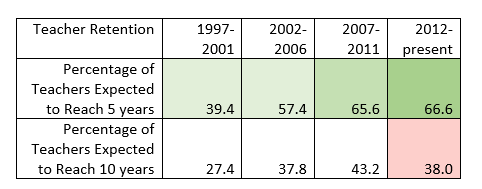

Using the Illinois retirement plan’s assumed rates, the following table shows the expected teacher retention rate in Illinois from 1997 to 2013. The data is based on the actuarial assumptions found in the Teachers’ Retirement System of the State of Illinois and TRS Comprehensive Annual Financial Reports. Although the data represent the plan’s assumptions for the future, not the actual rate, the assumptions are based on semi-regular experience studies that look at recent historical trends.

Illinois Teacher Retention, 1997 - 2013

Looking across the years, there is an increase in the expected retention rates from 1997 to 2012. From 1997 to 2001, the plan assumed only 39 percent of teachers would remain after five years. In 2002 to 2006, the plan readjusted its assumptions and expected 57 percent teachers to remain after five years. Based on experience study data indicating decreased withdrawal rates (or increased retention), the state teacher retirement plan further increased its 5-year retention expectations to 66 percent retention from 2007 to 2011. According to the experience study, the state actuaries underesitmated teacher retention and incorrectly “predicted too many terminations at younger ages.” In 2007, another experience study found that the state’s actuarial assumptions again predicted fewer terminations and recommend adjusting assumptions to reflect the increased retention rates. Today, the plan assumes approximately 67 percent teachers will remain for at least five years.

For Illinois, rising retention rates however translated to increasing costs, and in 2011, the state responded to these increasing costs by increasing the vesting requirement from five to 10 years. Using present-day assumption rates, this means that rather than 67 percent (the expected rate of teachers staying for five years) teachers vesting into the pension system, only 38 percent (the expected rate of teachers staying for 10 years) are expected to qualify for a pension. Raising the vesting requirement has more than compensated for the rise in teacher retention rates.

Illinois certainly has an onerous fiscal situation that needs to be addressed. The state’s situation is neither desirable nor sustainable. The Teachers’ Retirement System of Illinois reports an unfunded liability of $53.5 billion, and Illinois recently passed legislation in December 2013 seeking to address the funding shortfall. State legislators should continue to take steps to ensure fiscal stability and health, but in doing so, they should also consider structural reforms to address larger inequities.

*While teachers employed in Chicago participate in the Chicago Teachers’ Pension Fund rather than the Illinois Teachers Retirement System, they still follow the same Tier 1 and Tier 2 vesting requirements. Retirement ages and service years differ slightly within the Chicago Teachers’ Pension Fund.

Unfortunately, underfunding pensions is an easy and often legal way to deal with budget pressures. In 2013, California paid less than half of its required pension contribution. Illinois has consistently shortchanged its pension system for decades. Recently, New Jersey Governor Chris Christie announced that the state will be cutting pension payments from $3.8 billion to $1.38 billion. Whether Christie's proposal is legal has yet to be determined as plan participants prepare to challenge the cuts in court.

Law professor Amy Monahan argues that states need better legal mechanisms to enforce full funding. Many states have what are called “fiscal constitutional requirements,” or provisions in state constitutions that dictate the bounds of legislative fiscal activity (i.e.: a balanced budget requirement). In her article, Monahan looks at eight states with fiscal constitutional requirements for pension funding. She finds these provisions are rarely enforced, and even these states with supposed constitutional requirements to make their pension payments were no more likely to make their contributions.

She diagnoses several complications that prevent constitutional requirements from being fully enforced: Notably, the lack of clear, specific language in the provisions themselves and the lack of judicial authority to force legislative action.

While many state fiscal constitutional requirements stipulate that the legislature maintain an “actuarially sound” pension plan, there is no precise definition for what “actuarially sound” means. As Monahan explains, states can finagle the assumptions underlying the calculation of the ARC to give the false impression that its plans are better funded than they really are. For example, plans can select their own rate of return, even if real returns are lower. The Illinois Teachers Retirement System assumes an 8.5 percent return, for example, but in 2012, the plan’s actual returns were only 0.76 percent. Monahan suggests that an outside party such as the Governmental Accounting Standards Board (GASB) or an independent actuary determine a standardized funding methodology for states to apply. In turn, a definition of sound funding and specific calculations should be included in a fiscal constitutional requirement.

Another issue is judicial authority. Courts often rule funding requirements are unenforceable because pension participants lack standing. Even if a plan fails to make its contributions in a given year, it likely doesn’t put current retirees at risk. It’s only over time, as politicians continue to skirt payments, that participants may be in danger of losing out.

Courts also lack the power to remedy a breach in funding. Monahan suggests that fiscal constitutional requirements for pension funding be amended to become self-executing (which courts generally recognize), so that no legislative action is required. Currently, state fiscal constitutional requirements for pension funding are vague enough that legislatures have wiggle room in how they are interpreted and implemented. With clearer instructions, and an explicit constitutional provision that the funding requirement is self-executing, states will be pressured to make their full payments. Additionally, many courts just don’t have the power to order money to be appropriated from the state treasury to pay pension costs. Monahan suggests instead that courts could declare an entire budget to be unconstitutional, forcing the legislature to draft a new budget with sufficient pension funding. Alternatively, she suggests that the constitution could be amended to expressly allow courts to issue a writ requiring the state treasury to appropriate the necessary funds.

A last complication to constitutional funding requirements is flexibility. In economically dire situations, it may be better for a state not to be constrained to funding requirements. Paying down a state’s pension debt may take away from other vital municipal and social services. But too often, states repeatedly put off plan funding, placing pensions last on budget priorities. Monahan recognizes this issue and suggests a compromise: a reduced required contribution if certain constitutionally-defined triggers are met, or allowing the legislature to override the fiscal constitutional requirement by a super-majority vote. Monhan’s suggestions could curb repeated underfunding while still giving lawmakers flexibility to respond to times of true economic duress.

Without a robust enforcement mechanism, many states end up shortchanging pension funding. It’s often easier to underfund pensions when budget dollars are scarce, and likewise to make generous political promises to current constituents without tax increases. Unlike pensions in the private sector, public sector pensions do not carry the statutory funding protections of the Employee Retirement Income Security Act (ERISA). Implementing a strong but flexible state legal mechanism may be one way to prevent legislatures from underfunding state pension plans.

Taxonomy:The New York Post recently wrote about Milt Pachter, an 84-year-old man who loves his job at the Port Authority—so much that he works for free. When Pachter reached the normal retirement age, he had the choice of continuing to work or retire with a pension. Although he was not ready to retire, if he continued working, he would actually be turning down money he could receive through the pension plan. He chose to accept his pension and continue working, only now as an unpaid volunteer.

Employers can benefit from workers like Pachter with expertise and the desire to remain in the labor force. The Post quoted him saying, “I like work. I like mentoring. I have a lot of institutional memory about things I handle and want to pass on.” Pensions currently act as a crude tool, pushing veteran teachers who, like Pachter have knowledge and expertise they want to share, out of schools.

Pachter’s situation provides a personal lens into pensions. As researchers have written, traditional pension systems “push” older workers toward earlier retirement. Pensions rely on formulas that dictate how much employees can receive once they reach the “normal retirement age.” This is a blunt instrument, and it often means legislators are selecting what they think is the appropriate age for all teachers to retire. But not all teachers want to retire at the same age.

Once an employee reaches retirement age, pension benefits are disbursed as an annuity, a fixed benefit that a worker receives every year starting at retirement until death. Every year that an employee chooses to work after reaching the normal retirement age is a forgone year of pension benefits. Teachers nearing their state’s normal retirement age consistently respond to this disincentive and leave the classroom to maximize their benefits.

Many older public teachers may want to stay in the classroom, but the bluntness of pensions doesn’t take teacher preference into account. According to the Urban Institute’s pension report card, 24 state teacher plans received an F on encouraging work at older ages. This causes a problem for individual teachers, who may wish to continue working, and likewise for schools, who could benefit from the skill and expertise veteran teachers bring to the classroom. Instead, pensions create a structure that highly incentivizes workers to leave once they pass the normal retirement age, and those nearing normal retirement to continue working (“pulling” or locking teachers into the classroom despite individual choice or burnout). Yet, a teacher past normal retirement who wishes to stay may be more effective in the classroom than one who drudges on waiting to hit normal retirement.

Pensions force workers like Milt Pachter who want to continue working to make a choice between working and earning a salary or not working and earning a pension that’s worth almost as much. Instead, states should consider retirement systems that better align with worker preference, and performance, without penalty.

Taxonomy: