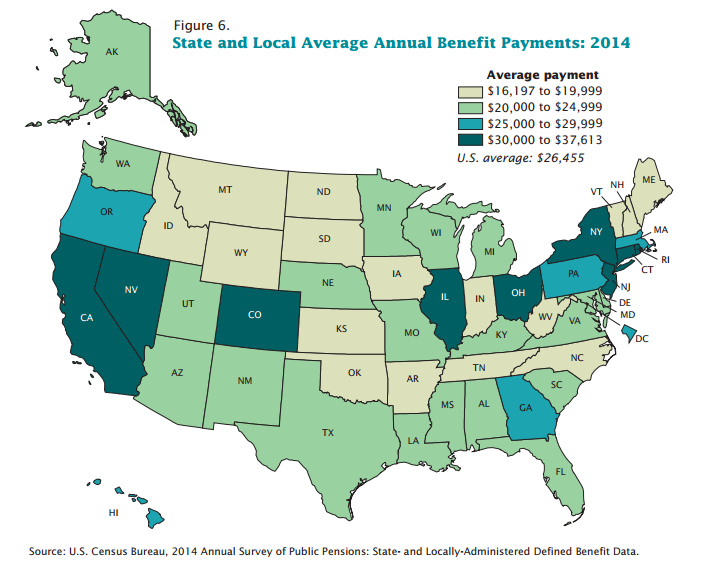

What does the "average" retired state or local government worker receive in pension benefits? The map below comes from the U.S. Census Bureau, and it shows the statistical mean pension benefit in each state. As the map suggests, average pension benefits tend to be highest in the Northeast and in Ohio, Illinois, Colorado, Nevada, and California. Benefits tend to be more modest in the Bible Belt and the Northern Rockies States of the Dakotas, Montana, Wyoming, and Idaho.

There are a few caveats to note about this map:

1. These figures are not adjusted based on cost of living. Although average pensions may be similar in Georgia and the District of Columbia, for example, these two places have different costs of living.

2. The figures do not factor in Social Security. Sticking with Georgia as an example, it does not offer all of its public-sector workers Social Security--its neighbors all do--so Georgia must offer more generous pension plans than neighboring states.

3. The pension figures also do not factor in the worker's own contributions. Even if workers earn the same pension amount, workers who contributed less toward those pensions will have higher net benefits.

4. Although the figures include public school teachers, they also include all other state and local government workers who qualify for public pension benefits. In our experience, retired teachers tend to earn slightly higher pensions than other types of public-sector employees, meaning the figures above under-state the average teacher pension.

5. These figures include all retirees earning a public-sector pension regardless of when they retired. For a variety of reasons--such as pension benefit enhancements states have enacted over time, salary increases that boost pension formulas, and cost-of-living-adjustments that don't keep up with inflation--the pensions of those who recently retired tend to be higher than those who retired years ago.

6. Perhaps most importantly, "averages" hide a lot of nuance. Our work suggests that about half of all new teachers won't stay long enough to qualify for a pension. Although these are public-sector workers, they won't show up in the pension benefit figues, because they won't have a pension at all. But even beyond that, the averages are distored by outliers on both ends of the spectrum. Lots of workers qualify for relatively small pensions and a small portion of workers qualify for much larger benefits. Those two extremes will artificially depress the "average" benefit. In Illinois and California, for example, the "average" pension was well below the median (middle) and mode (most common) benefit amounts.

We've been working to compile teacher-specific figures, but in the meantime, remember to dig beyond simple averages to look at the full distribution of retirement benefits. In our experience, there are significant inequities depending on when teachers start, what state and even what district they work in, whether they cross state lines, and how long they remain teaching.

Taxonomy:What's causing teacher shortages across the country? Although it might be fun to blame your least favorite thing in education--the Common Core, say, or teacher evaluations or millennials--new research suggests the economy is the primary driver in the supply of new teachers (h/t InsideHigherEd).

The paper looks at the college majors of students who turned age 20 between 1960 and 2011. Then, it linked the students' decisions with data on macroeconomic trends to examine how business cycles affect student choices. Of the 38 majors included in the study, education was the biggest loser. When recessions hit, both men and women were less likely to want to become teachers and instead turned to fields like accounting and engineering. In number terms, the researchers estimate that, "each percentage point increase in the unemployment rate...decreases the share of women choosing Early and Elementary Education by a little more than 6 percent." (For men it was even higher.)

To put that in context, the national unemployment rate rose from 4.4 percent in May 2007 to 10.0 percent in October 2009. Using the paper's estimates, that would imply the recent recession caused a decline in female enrollment in elementary education of 33.6 percent (the 5.6 percentage point change in the unemployment rate multiplied by the 6 percent figure above).

A 34 percent decline due purely to economic conditions may sound high at first blush, but it does help explain much of what we're seeing out in the field. For example, it would explain most but not all of the decline in program completers that we documented in our recent paper on California's teacher pipeline. State-by-state changes in economic conditions may also help explain why some, but not all, states are experiencing declining interest in teacher preparation programs. (And all of these figures put Teach for America's much-publicized 10 percent decline in perspective. So far, TFA has weathered the decline better than other preparation programs.)

While the declines are not good news for schools--it means they're competing for a smaller number of candidates--a recent paper found that teachers hired during the recent recession tended to be stronger than those hired during better economic times.

What's ironic about all current attention to teacher shortages is that teacher shortages are the exact thing that will lead to the next boomlet in teacher prep. The media will cover the shortages, districts will raise their wages to attract workers, and we'll start this cyle all over again. And then the next recession will hit and we'll be back to hearing about teachers who can't find teaching jobs. And so on, and on...

Taxonomy:New Jersey Governor Chris Christie certainly doesn’t beat around the bush. In an interview with Jake Tapper, New Jersey Governor said he prefers to deal with bullies with a “punch in the face.” Who deserves this? The teachers’ unions, according to Christie.

While this sort of brash talk may attract attention, it isn’t good for negotiating reform. Ironically, Christie actually has a good reform proposal. Christie’s pension committee calls for a cash balance plan, a type of defined benefit plan that accrues benefits evenly rather than the bumpy accrual of the current backloaded plan. The cash balance plan would provide better benefits for early and mid-career teachers who get shortchanged by the current plan and better fiscal housekeeping for the system.

But Christie’s politics are preventing this reform from moving forward. The teachers’ unions are still fuming over the Governor’s decision to go back on his promise and shortchange the pension fund.

As Christie continues to play with fire, however, he may stymie the state’s chance for genuine reform of its pension systems.

Taxonomy:California’s pension debt is dizzying. The state’s collective unpaid pension debt is now $198 billion, up from $6.3 billion in 2003. The California Teachers’ Retirement System (CalSTRS) makes up over a third of this debt, $74 billion unfunded. (These numbers look even bigger depending on what discount or interest rates are used.)

Complicating matters, the state can’t reduce any future benefits under an obscure, rigid legal doctrine known as the California Rule. Under the rule, workers are basically promised the same (or better) benefits as laid out on their first day of work; workers get what they’ve earned so far as well as future earnings. (A new ballot initiative may allow for structural reform and better public accountability, but is still up in the air.)

Put this together and it means that a younger generation of workers are stuck with the state’s massive bill. As we write in our new TeacherPensions.org report, pension reform cuts typically fall on new workers, and now is the worst time in the past three decades to be a new teacher.

Check out TeacherPensions.org resources and past blogs for more info on California, including interviews with former San Jose Mayor Chuck Reed and current Executive Director of the California School Employees Association, Dave Low.

Taxonomy:Over half of new teachers won’t meet the minimum vesting or service requirements to receive a pension. One common response is that these teachers are allowed to receive a refund on their contributions plus interest, and that the refund is comparable to private sector workers who receive a 401k. It’s a good point, but it’s not exactly the case for all teachers.

While it’s true a teacher can get a refund on her pension contributions plus interest in some states, like California, in other states, like Illinois, teachers do not receive interest. In fact, in Illinois, teachers receive less than their original employee contributions. An Illinois teacher is required to contribute 9.4 percent of her paycheck to the state teachers’ retirement system. Upon leaving the classroom, however, she is only entitled to a refund equal to 8.4 percent of her earnings. And, in the majority of states, teachers do not receive any portion of their employer’s contributions.

Overall, state public retirement systems face significantly less scrutiny from the federal government than the private sector. Unlike the private sector, states are not required to provide their public workers with Social Security, can set their minimum vesting requirements upwards of 10 years, and aren’t held to the same funding standards. So California teachers may be able to get a full refund with 4.5 percent interest, but they also won’t get Social Security. For teachers in Illinois, they receive neither a full refund on their pension contributions nor Social Security for their time in the classroom. Not all teachers are eligible for full a refund, and there are other trade-offs for participating in the state system to consider.

Participating in the state systems may be good for a select few, but for the majority of teachers, it comes with too many trade-offs.

It’s back to square one for Chicago pensions: last Friday a city judge ruled unconstitutional a pension law that would have reduced benefits for city workers. The ruling is a tough blow for the city’s finances and could worsen the situation for new and future workers, including teachers.

For Illinois taxpayers, it feels a lot like Groundhog Day. Chicago’s pension reform law, albeit a slightly different spin, like the state’s 2013 pension reform law, attempted to reduce cost-of-living adjustments for current workers. And like the state law, the city court says the cuts violate the state’s constitution. Even if the case goes to appeal, it’s highly likely that the city’s attempt to cut benefits will again be deemed illegal just like the state’s attempt, which was finally upheld as unconstitutional last spring.

Paying the price for massive debt are the city’s workers. On the books, the city judge’s ruling is a win for the Chicago Teachers’ Union and other unions who filed the suit. But it’s a significant loss overall for the city’s new and future workers and teachers who need to continue eating the costs of growing debt. Chicago, like the state, already instituted drastic cuts for its new teachers through a previous plan in 2011. New teachers hired after 2011 face negative net benefits for the first two decades of work because the value of their contributions exceed their future pension benefits. And they don’t qualify for Social Security. For the city’s schools, last year’s pension contributions ate up 11 percent of the Chicago Public Schools’ operating budget, or nearly $1,600 per student.

Chicago is running out of options. Without the pension law, which would have allowed the court to enforce full funding to the laborer’s and municipal employees funds, the city lacks any checks to ensure adequate funding. Moody’s recently downgraded the Chicago Public Schools’ debt rating to junk status, now matching the city’s rating, because of poorly funded pensions; the S&P cut the city’s rating again because of chronic structural debt. Governor Bruce Rauner’s recent pension bill would allow Chicago and other municipalities to file for bankruptcy, a mechanism which would allow the city to start over, restructure its past debt, and reform its pensions plans (but even in this case, there would be obstacles around when Chicago could actually file because of the way the city reports its debt).

The city desperately needs structural reform to clean up its financial mess and to ensure adequate benefits for its teachers and municipal workers. Until then, Chicago’s public workers, teachers, and taxpayers will be expected to foot the bill.