There’s been a persistent myth that when it comes to retirement plans, “pension" means "better.” Hearing the word "pension," many people are led to believe this means a secure and comfortable retirement. After all, pensions mean a guaranteed lifetime annuity. The Seattle Times even recently published an article listing the last few jobs that still offer traditional pensions, as a way for jobseekers to scoop up positions that offer these supposedly better retirement plans.

But the big error in reasoning, here, lies in the fact that not all pensions are equal. A worker might be promised a pension for life, but the amount of that benefit varies greatly, depending on her years of service.

Take a look at the net pension benefits, after a teacher’s own contributions, for a teacher in Colorado. Teachers who work for five to even 20 years receive relatively little net benefit. The orange and yellow shading take up only a small slice of benefits, compared to the mountain of benefits earned by a teacher who stays for thirty plus years. Can’t see the sliver of orange very well? That's because early career teachers earn minimal benefits based on their low years of service, lower salaries, and delay in collecting benefits until years later when benefits have eroded away from inflation. In terms of dollars, a teacher who works in the classroom for a total of five year earns a lifetime net benefit worth about $6,800 in today’s dollars, whereas a teacher with 35 years earn a benefit of over $680,000—a hundred times what the early career teacher earns.

Net Pension Benefits for Teachers in Colorado

Source: Chad Aldeman and Michelle Welch, “Few Reach the Peaks,” TeacherPensions.org, 2015.

When people think of pensions as reliable and ample retirement income, they’re really thinking of the blue part of the graph. But in reality, only a small minority of workers actually reach this level of wealth. In Colorado, only 7 percent of teachers are expected to remain in the classroom for 30 years and reach peak benefits, according to plan assumptions. The majority of teachers, on the other hand, more likely will have benefits closer to the orange or maybe yellow section on the graph. To make matters worse, 40 percent of all public school teachers, including those teaching in Colorado, are not eligible to participate in Social Security, placing even more weight on a system that isn’t serving the majority of its members well. (Most people don’t realize that many teachers are uncovered, and this fact failed to make the rose-colored job list posted by the Seattle Times.) Pensions are supposed to be the mainstay for retirement, but few will get adequate benefits and instead will have to rely on other sources of income or work longer to ensure a secure retirement.

And this isn’t just a problem in Colorado. The majority of states place teachers--and public sector workers in general--in traditional pension plans that have the same backloaded structure. In New York, for example, benefits accrue in such an uneven pattern that teachers earn roughly $3,500 per year of work for the first 20 years of service while earning $30,000 per year for teaching years 30 through 38. In Illinois, net pension benefits are actually negative for a 25-year-old teacher who teaches anything less than 26 years. Meanwhile, an Illinois teacher who stays for a total of 30 years receives a net lifetime pension benefit of $389,000. In California, teachers earn negative benefits during the first two decades of work, but a teacher who works for 40 years will receive an annual pension of over $90,000.

Granted, this isn’t to say that career teachers shouldn’t earn greater pension benefits. Veteran teachers who remain in the classroom for 30 plus years should be rewarded for their long-term commitment to the profession and their students. But, the magnitude of inequity and disproportionate allocation of benefits in the current system warrants a policy change.

The next time you hear the word “pension,” think twice before jumping to any conclusions. Because for most people, a pension unfortunately won’t lead to a cushy retirement.

Taxonomy:To illustrate the ways pension plans create incentives for teachers, I created a list of things teachers would do if their sole motivation was maximizing their pensions. Of course teachers have many competing motives, and not all of these steps are feasible, practical, or ideal for all teachers, but here are eight ways they could legally boost their pensions:

- Stay in school: This one may seem obvious, but the key to maximizing a pension is to stay in the pension plan as long as possible, or at least until you reach the plan's "normal retirement age," usually around age 60. Don't take time off or leave the profession for any reason, because any lost years won't count toward your pension plan's "years of service" calculation.

- Don't leave your state. It's no good to split a teaching career across state lines (or even across different pension plans in the same state). One study estimated that a teacher working a 30-year career in the same state had two or even three times the pension wealth as a teacher with the same 30-year career who split her time across two states. So if your spouse wants to move, or if you want to be closer to family or just try a new career, know that you're sacrificing your retirement.

- Earn as little as possible for as long as possible. Every state requires teachers to contribute some portion of their salaries into the pension plan. To maximize the net return on their pensions, teachers should want to keep those contributions as low as possible.

- Become a principal (or a superintendent). Ideally, teachers would keep their low salaries (and low pension contributions) for almost all of their career. Because pension formulas are typically based on the employee's highest three or five years of salary, they should try to do everything in their power to make their peak earning years count. The best way to do that is to pursue higher-paying jobs as principals or administrators. Teachers need to get out of the classroom if they really want to maximize their pension.

- Move to a suburban district right before you retire. Again, a teacher seeking to maximize their net pension wealth should stay in a low-salary district for as long as possible, but right before retirement they should seek out the wealthiest district possible. Just a few years of earning the higher salary will pay big dividends in the form of higher pension payments every year in retirement. (The slightly higher pension contributions in those years are more than compensated by the higher pension payments.)

- Be a woman. Women live longer, meaning they have, on average, more years in retirement to collect a pension.

- Store up your sick leave and vacation days. Many states allow teachers to "cash out" their sick leave and vacation days when they retire, artificially inflating their salary in that year. Even better, that inflated salary will translate into higher pension payments for life. So as you're nearing retirement, try not to get sick or take vacation time.

- Retire when the state tells you to. State legislators set the "normal retirement age" for teachers, and that's when they want you to retire. If at that point you decide you still like teaching, every year you keep working is a year you could be receiving a pension. You're losing out.

If you read this list and think it doesn't quite square with why you went into teaching, your pension plan may not be working in your best interests (or the best interest of schools and students). It may be time to consider other options.

- Public sector unions can breathe a sigh of relief after Friday’s state Supreme Court ruling: an Illinois pension reform law that would have cut benefits for existing workers was declared unconstitutional. Meanwhile, policymakers are back to the drawing board, but this time their options are much more limited.We already got a preview to the court’s view on benefits in an earlier case, Kanerva v. Weems, where the court ruled that retiree health care benefits are constitutionally protected. And health benefits aren’t even explicitly mentioned in the state’s constitutional pension clause. But if you had just looked at the court’s stats, you may have been inclined to double down on a reversal. The Illinois Supreme Court has reversed or reversed in part over half of its cases while only affirming about 40 percent. But they also tend to vote unanimously. And if you heard the skeptical questions from the justices during oral arguments, today’s conclusion comes as no surprise.What’s next? The state faces an unfunded liability of over $100 billion across its five different retirement systems, and pension benefits have already been cut down to the bone for new workers. For teachers in the current system, a newly hired 25-year old would need to work until age 51 simply to make a positive return on her contributions; in other words, a new teacher’s benefits are negative for the first 25 plus years of service. Keeping benefits ironclad may be a win for senior union leadership, but it’s a loss for new and future workers who will now bear the full brunt of cuts.It would be a fool’s errand for current Governor Rauner to attempt, once again, to reduce benefits of current workers with the current pension clause in place. Why states like Illinois and New Jersey continually pick legal fights with public sector unions on pension benefits to begin with is a mystery, and an expensive one at that. But Illinois is beyond tweaks and trims; the state needs a comprehensive structural reform, and filing for bankruptcy isn’t a viable option for a state. A constitutional amendment could loosen the current rigidity in the system. But even so, Illinois’ teachers remain without Social Security in addition to insufficient pension benefits.Moving forward:

- Illinois first and foremost must find a way to responsibly deal with existing debt.

- At the same time, the state should consider placing all new workers into a new plan that is more predictable for the state while providing workers with adequate retirement benefits that includes Social Security. Possible alternative plans could include a cash balance, hybrid, or a well-structured 401k plan.

- But the state should give existing workers the choice to opt into the plan, rather than requiring it and thereby avoid another legal battle.

Illinois future teachers need benefits that will put them on a path to a secure retirement, and policymakers need to act quickly.Taxonomy: There may be a new kid on the block for American private-sector pensions. Something called a “composite” pension plan has entered the scene as a new alternative to traditional defined benefit and defined contribution plans.

Last week, the House Education and Workforce committee held a hearing to consider the merits of composite plans for multiemployer pension plans. According to the Department of Labor, there are 2,740 multiemployer pension plans (about half of which are defined benefit plans) covering over 15 million private workers and holding $624 billion in assets. Multiemployer pension plans made headlines last fall when the PBGC—an independent government agency that insures private pension plans—announced that multiemployer plans had a $42.4 billion deficit and many will likely run dry in the next ten years, prompting Congressional action. PBGC estimates that up to 10 percent of the 1,427 multiemployer defined benefit plans are likely to become insolvent.

Modeled after Canadian target and lesser-known variable benefit plans, the proposed composite plans could help address some of the funding challenges facing multiemployer plans. Here’s how they work:

- Composite plans currently have no legal category, but presumably seek to retain the better elements of a defined benefit while promoting better funding discipline and the predictable employer costs of a defined contribution plan.

- Under a composite plan, workers would receive a lifetime annuity. Assets and longevity risks would be pooled as they are in current multiemployer defined benefit plans and so would expect higher benefits than 401k or defined contribution plans.

- However, benefits would be tied to the plan’s performance so employees would share some of the risk alongside employers. Plans would set threshold or "hurdle" rate based on a conservative investment return. If a plan equals the hurdle rate, the plan basically functions the same as a traditional defined benefit pension plan. But if a plan’s investment rises above or falls below the hurdle rate, then benefits get boosted or decreased accordingly.

- Workers are guaranteed a floor of lifelong benefits and so won’t risk outliving their benefits. Unlike a traditional pension plan, however, the the exact amount of benefits isn’t promised ahead of time.

- The recommended composite plans would require 120 percent funding of actuarial projected cost of benefits. Boosting benefits would be closely tied to the plan’s funding, so employers can’t make generous promises that they can’t keep. If a plan falls below 100 percent funding, benefits would also drop, thereby incentivizing workers to ensure full funding through collective bargaining.

There are definitely some good qualities about composite plans. They would ensure better funding discipline and provide a buffer against economic downturns by allowing employers to adjust benefits, while still guaranteeing workers lifelong benefits. So far they have bipartisan as well as labor union support, a rare combination. But a big piece missing from the discussion is equity. The proposed composite plans suggest they will use similar back-loaded formulae as traditional pension plans, leaving younger workers who don’t stay for a full career vulnerable to retirement insecurity. Reformers should consider including other design levers to avoid the problematic back-loading of traditional pensions alongside the flexibility and funding discipline offered by composite plans.Taxonomy:Pensions are not just about state budgets and numbers with lots of 0's behind them. Pensions affect real people, and our work here at TeacherPensions.org attempts to explain the ways in which complicated pension issues trickle down and affect the lives of millions of teachers. So when I was asked to give a presentation on pensions at the Education Writer's Association (EWA) 2015 National Seminar, I wanted to use the opportunity to suggest ways education reporters can dig into pension issues in their state. Here are 10 potential story ideas:

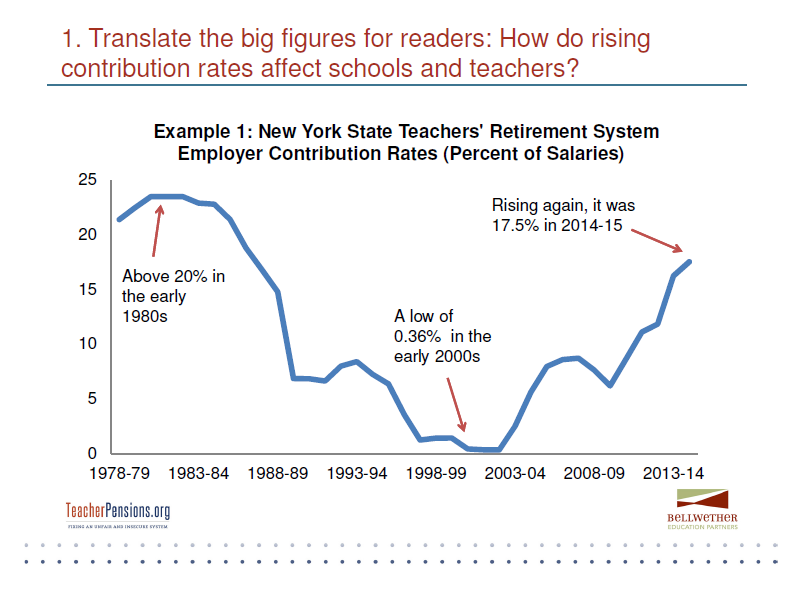

1. How are pension costs affecting your state's schools? Pension costs usually don't appear on the education beat, but that doesn't mean pension funding doesn't affect schools. There's wide variation across states, but nationally retirement costs eat up more than 19 percent of teacher compensation. That figure is rising fast, much faster than in other professions. The chart below helps illustrate what it looks like in New York state. Reporters could be asking things like how school district leaders are making budgetary choices or whether teachers know how much money is being contributed on their behalf.

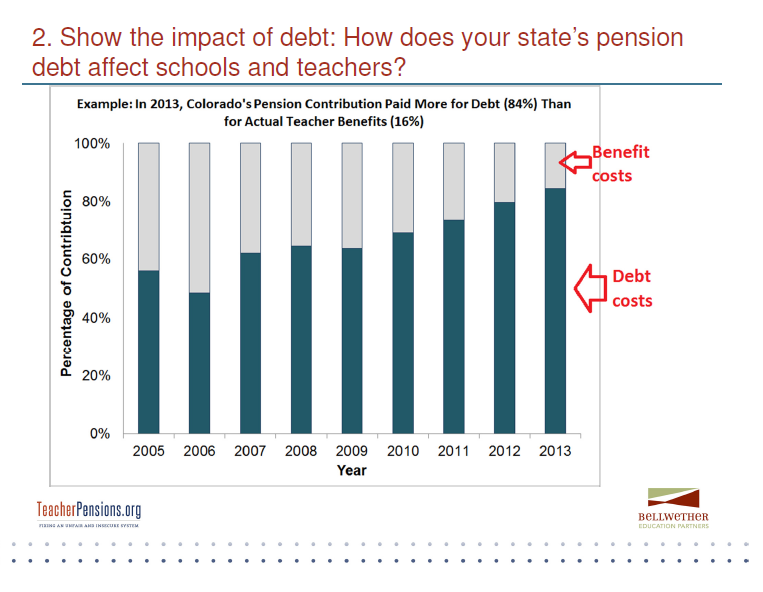

2. What does it mean when a state pension plan has an "unfunded liability?" For budget people, it means the state needs to find new money. But just like other forms of debt, pension debt carries real costs for schools and teachers. As contributions to pension plans are rising, the majority of contributions today are actually going to pay down accrued debt. Nationally, for every $1 that states and schools are contributing to pensions, 70 cents goes toward paying down debt and only 30 cents goes toward actual teacher benefits. The chart below presents an example from Colorado, where 84 percent of today's contributions are going toward debt and oly 14 percent toward teacher benefits.

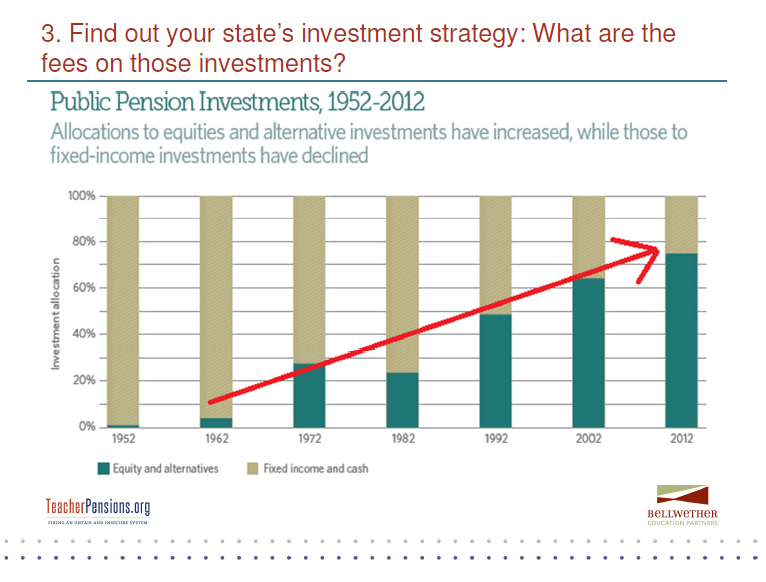

3. Pension plan investments have been in the news recently, but what is your state's investment plan? Most states assume they can earn a 7.5 or 8 percent return on their investments, and states have systematically increased their exposure to stock markets and private equity. The chart below comes from the Pew Center on the States, and it shows how states have over time increased their exposure to risky assets. What does this look like in your state?

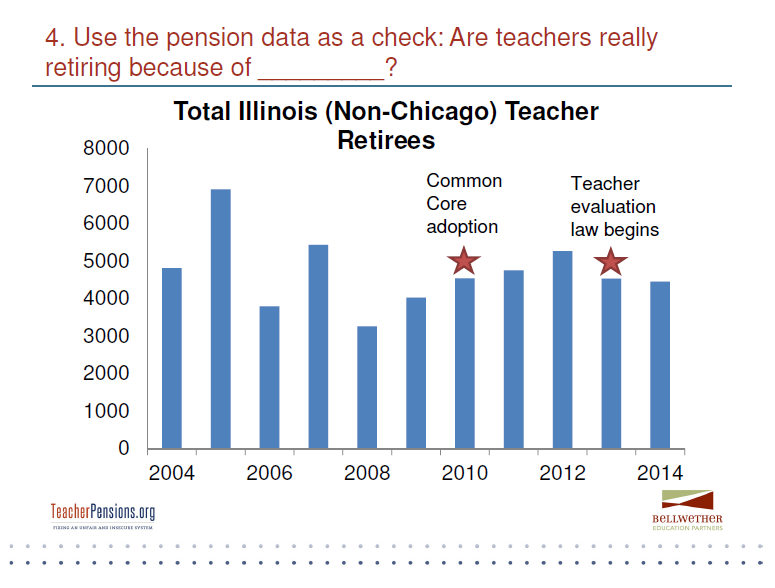

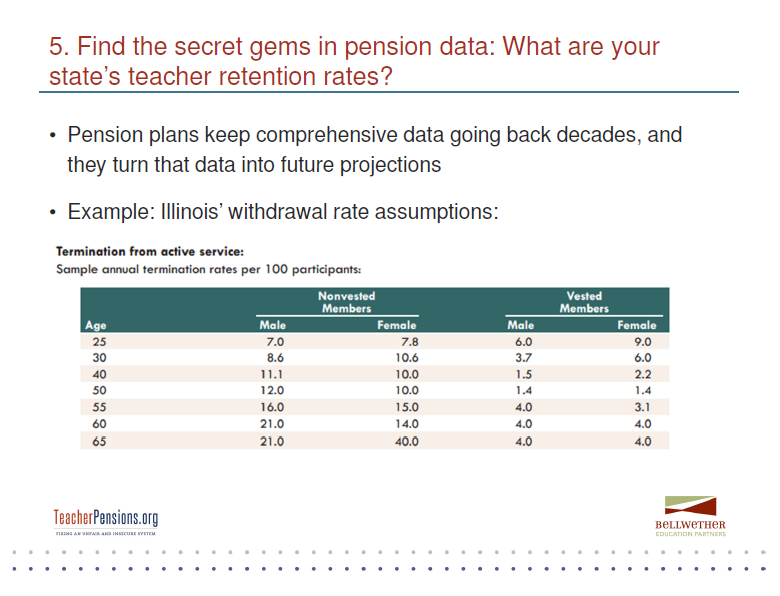

4. Pension plans are a great, untapped source of data. In order to pay benefits down the road, pension plans have to keep impeccable records about their enrolled teachers, including how long they stay in the profession, how much money they earn, and when they retire. The next time there's a story about rising or falling teacher retention or retirement rates because of X, check the pension plan data to make sure this is reality. The graph below pulls in 10 years of retirement data from the state of Illinois. Although there may be certain teachers leaving the profession in Illinois because of things like the Common Core (adopted in 2010) or new teacher evaluations (implemented in 2013), the data do not support the notion that waves of teachers are retiring because of these developments.

5. Pension plans are a treasure trove of data even for things like teacher retention rates. In order to estimate how much money they'll need to pay benefits down the road, pension plans make assumptions about how long teachers will stay in the profession. (Every few years they test their assumptions against their actual observed data.) We've used those projections to estimate how many teachers will stay for 5, 10, or even 30 years. Reporters could run similar calculations to let readers know how their state compares.

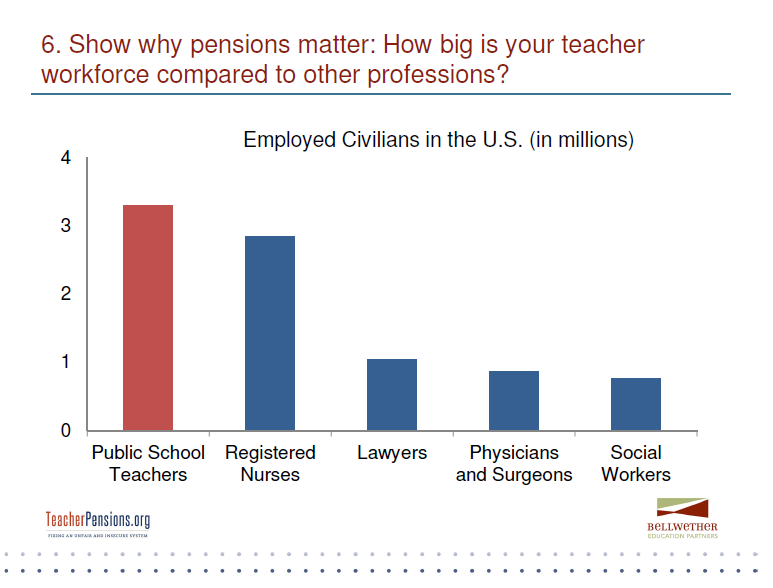

6. Education news coverage can occasionally get lost in a vacuum. It's important to remind readers just how big and important the teaching profession is to this country and to individual states. With more than 3 million public school teachers, they're the largest class of college-educated workers nationwide (and probably in your state as well.) Things like how well teacher retirement plan are working is not just an issue for individual teachers--they're also a big part of state economies and it matters whether they have sufficient retirement savings.

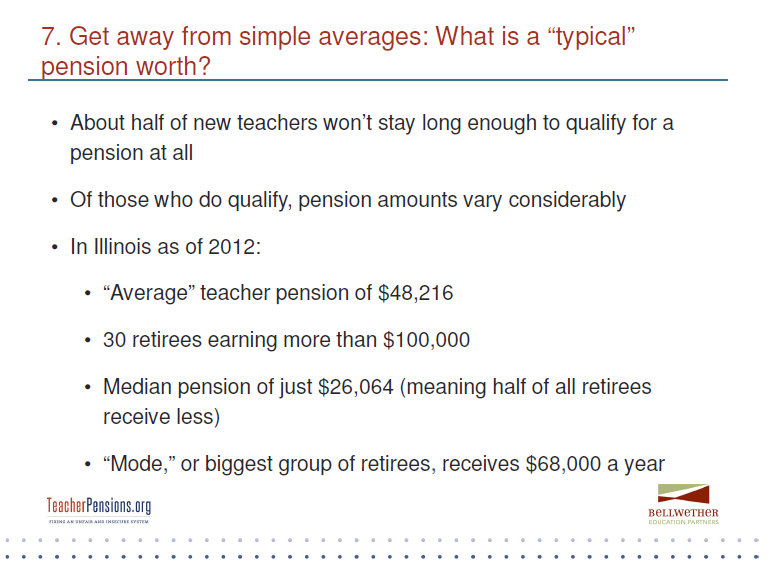

7. Reporters should steer away from reporting the simple "average" teacher pension plan, because the average hides a lot of nuance. As we've estimated, about half of new teachers won't qualify for a pension at all. They won't earn a pension and will leave their public service without any employer-provided retirement benefit. Even among those who do earn a pension, the amount will vary tremendously. As a reporter, try to find individuals who represent all sides of this story, not just the few lucky ones who qualify for the best, "gold-plated" pensions. Tell the story of all the different types of people who work in your state's public schools (there are great examples here).

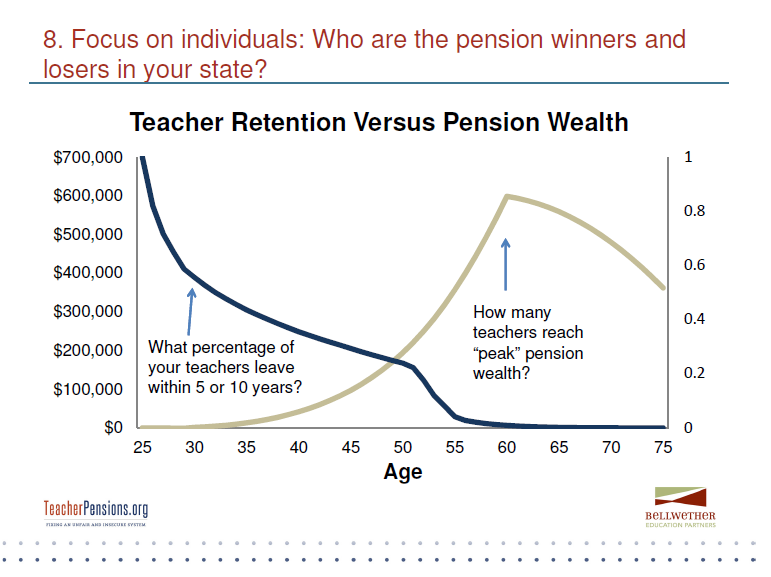

8. Reporters should make sure the story is about individuals. That will make for a more compelling story and do a better job enlightening readers about how your state's pension plan is (or is not) providing secure retirement benefits to all teachers. The chart below shows the rate at which teachers leave the typical state (the dark blue line) set against the rate at which they earn retirement benefits (the tan line). Does your state have this divergence between the number of teachers who stick around and the amount of benefits they earn? How does your state compare to other states? Do teachers know when and how they earn pension benefits, and do they change their behavior accordingly?

9. The best news stories have some tension. There are tensions at play in teacher pension plans. Because pension plans reward those who stick around in one place for a long time, they let younger, more mobile workers subsidize older and more stable workers. And because pension plans are based on a formula that factors in salary levels, employees with higher salaries (like district superintendents and administrators) tend to earn disproportionately large benefits compared to teachers.

10. Nowhere do tensions play out more than in the generational divide. Because states have moral and sometimes legal protections against changing retirement benefits for existing workers, when states are pressed into tough budget climates they are forced to adopt particularly steep cuts on new and future teachers. They do this through the creation of new "tiers" where workers hired after a certain date are placed in a different, worse plan than those who came before them. Nearly every state has multiple tiers now. Teachers may be working side-by-side in the same school, and paying the same contribution rates, but earning very different retirement benefits. Do teachers know about this? How do new teachers feel about subsidizing the retirements of other teachers? What about teachers hired just on or before the date when the old tier started and the new one began? Will this affect the teaching profession writ large, making it harder to attract and retain good teachers?

Those are just some of my ideas. For any reporter interested in more information, or to talk through their own story ideas, please feel free to email me at chad-dot-aldeman-at-bellwethereducation-dot-org.

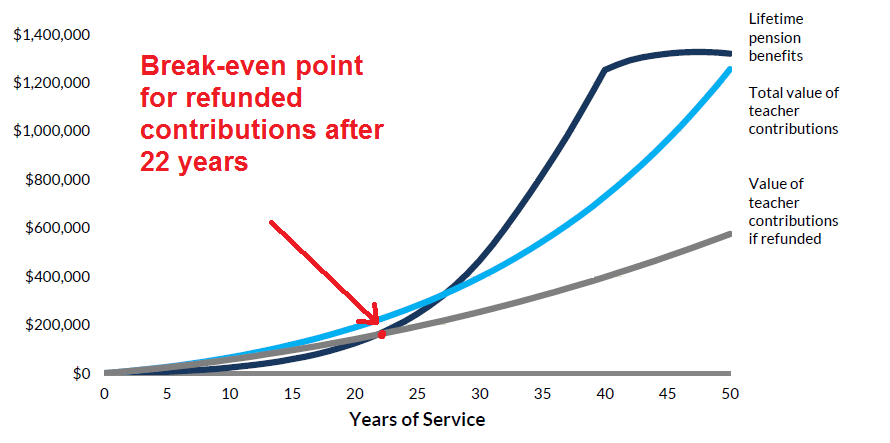

- After spotting a deal that looked too good to pass up, you discover a flaw and end up returning and getting a refund on your purchase. It may sound shocking and counterintuitive, but in many cases, teachers may actually be in a similar situation with their pension plans. They might be better off taking a refund on their contributions rather than waiting around to receive a pension.How is this possible? Teachers qualify for very little in the way of retirement benefits during the first half of their career because pension benefits don’t accrue evenly. A mid-career teacher therefore is faced with a choice: she qualifies for some pension and can receive lifelong payments upon retirement, or she can forfeit her rights and get a refund on her contributions.New research from the Urban Institute compares the value of a teacher’s contributions to a teacher’s overall pension wealth. Using the pension plan’s own interest assumptions (often 8 percent), in half of states teachers need to stay in a single system for at least 24 years to simply break even on their contributions plus interest. Even using a more conservative 5 percent interest rate, a teacher would need to stay for at least 15 years in order to break even in the median state. This means that an individual teacher could work for over a decade, diligently contributing to the system, and qualify for a pension that’s worth less than the value of her own contributions plus interest. She may actually lose money to the state pension system.The graph below shows the differences in the value of a newly hired, 25-year-old California teacher’s lifetime pension benefits, her contributions using the plan’s interest assumptions (7.5 percent interest), and her contributions if the teacher requested a refund. Although California assumes it can earn 7.5 percent interest every year on the plan’s assets, the state plan only gives teachers 4.5 percent interest on refunded contributions. For a new California teacher, even the limited refund policy would be worth more than her actual lifetime pension benefits for the first 22 years of her career. She would be better off getting a refund and giving up the pension if she teaches for anything less than 22 years.The Value of a Teacher's Contributions Versus Future Benefits

Source: Richard Johnson and Benjamin Southgate, “Can California Teacher Pensions Be Distributed More Fairly,” Urban Institute, October 2014.

Refunding and rolling over her contributions to a tax-sheltered savings vehicle would actually allow that teacher to grow and invest her contributions, rather than giving it up to the state and waiting the years before she can actually collect a retirement pension, whereupon its value has eroded over time. Most state pension formulas, including California’s, don’t adjust salary figures for inflation when calculating benefits. A teacher, of course, has to weigh the risks and her own savings habits; if she is prone to high spending or making risky purchases where she burns through all her contribution money rather than saving, otherwise known as “leakage,” then keeping it locked away with the state in exchange for a small pension down the road may be a better decision.On the surface, a lifelong annuity sounds like a great deal. In California, the plan assumes that less than a quarter of teachers with 15 years of experience will take a refund. In other words, the plan assumes that most teachers who qualify for a pension usually take it. But not all pensions are equal, and for many teachers, pensions likely carry a flaw that demands a refund. The reality is that pensions vary vastly depending on how many years of service a teacher has and when she can actually retire and collect. Just because a teacher has the option to get a pension at some point down the road doesn’t necessarily mean she should take it.*This is post is based on research on California’s teacher retirement plan. It is not personal or institutional investment advice. Please consult a qualified financial professional before making consequential financial decisions.